Your lender just sent foreclosure papers. Now what? Here's something most homeowners don't realize: receiving a foreclosure notice isn't the end of the road. You've still got moves to make—some can buy you months, others might stop the foreclosure completely.

What matters now? Understanding which defenses work for your specific situation and acting before your window closes.

Understanding Your Foreclosure Defense Options

Where you live changes everything about how foreclosure works. Judicial foreclosure states—places like Florida, New York, and Illinois—require lenders to sue you in court before taking your home. That lawsuit opens doors: you can force the lender to prove their case, challenge their evidence, and raise defenses that might kill the foreclosure entirely.

Non-judicial states like California, Texas, and Arizona? Different ballgame. Lenders use a trustee to foreclose without ever seeing a judge. The timeline compresses—sometimes dramatically. You'll receive statutory notices, but there's no automatic court hearing where you can present defenses. Want to challenge the foreclosure? You'll need to file your own lawsuit and convince a judge to issue an emergency order stopping the sale.

Here's what most people miss: the calendar controls your options. Got a fresh default notice? You've got breathing room to negotiate a workout, apply for modification, or explore alternatives. Already received a lawsuit or notice of sale? The clock's ticking—your focus shifts to legal strategies and emergency measures. Sale date set for next month? Your choices narrow fast, though bankruptcy can still slam the brakes on at the last second.

Know the difference between buying time and actually winning. Filing an answer to the foreclosure lawsuit? That delays things while you fight, but it doesn't make your missed payments disappear. Proving the lender lacks legal standing to foreclose? That's a potential knockout punch that could end their case permanently.

Timelines vary wildly. A judicial foreclosure in New York might drag on 800+ days from first missed payment to auction. Nevada's non-judicial process? Could be done in 120 days. These windows determine how much runway you have.

How to Fight Foreclosure Using Legal Challenges

Legal defenses target the foundation of the lender's case. Win on these issues, and you don't just delay—you potentially stop the foreclosure cold or create serious leverage for settlement.

Challenging the Lender's Standing to Foreclose

Here's a question that derails thousands of foreclosures every year: does the company suing you actually own your loan? During the 2000s housing boom, mortgages got bought and sold like baseball cards. Your loan might have been originated by Countrywide, sold to Bank of America, transferred to a securitization trust, then serviced by Nationstar. Each transfer should have been documented properly. Often? It wasn't.

The foreclosing party needs to prove they own your promissory note and mortgage through an unbroken chain. Missing links kill their case. An assignment dated after the lawsuit started? Problem. Endorsement on the note missing a required signature? Bigger problem. Assignment from a company that dissolved three years before the document was supposedly signed? You get the idea.

Courts don't take this lightly. A 2023 case out of Tampa resulted in dismissal because the plaintiff showed up with a note bearing an endorsement that didn't match any assignment in the record. The homeowner stayed put. The bank had to reconstruct the entire chain of ownership—a process that burned 14 months and counting when last reported.

Your move? Pull every assignment from your county's official records. Scrutinize signatures—were they signed by "assistant secretaries" at companies that used robo-signing mills? Check dates against the foreclosure timeline. Look for assignments from entities that had already gone bankrupt. County recorder websites make this easier than you'd think.

Author: Olivia Carringt;

Source: redmonpestmgt.com

Identifying Predatory Lending Violations

Predatory lending defense attacks what happened when you got the loan. Federal and state laws prohibit specific abusive practices. Violations don't just provide defenses—they can sometimes offset what you owe.

What counts as predatory? Truth in Lending Act violations, like failing to provide accurate APR disclosures. Steering you into a subprime loan when your credit qualified for prime rates. Charging points and fees exceeding legal limits. Misrepresenting whether your payment included escrow. The Home Ownership and Equity Protection Act adds extra requirements for high-cost mortgages—violations there carry serious consequences.

Timing complicates things. TILA claims typically must be filed within one year of closing. But wait—some courts allow these violations as defenses to foreclosure even outside that window, treating them as reasons the debt shouldn't be enforced as written. State consumer protection laws often have longer limitation periods and may allow loan rescission.

Dig up everything from your loan closing: the initial Truth in Lending disclosure, Good Faith Estimate, all the forms you signed, notes from conversations with the loan officer. Compare what you were promised against what the actual mortgage says. Significant differences? That's ammunition.

Wrongful Foreclosure Claims and When They Apply

Wrongful foreclosure happens when lenders foreclose despite not having legal grounds or while violating procedural rules. This differs from standing—you're not questioning whether they own the loan, but whether they foreclosed properly.

Classic examples: proceeding with foreclosure while your modification application sat pending review (called "dual tracking"—illegal under Dodd-Frank). Skipping required notices. Calculating the default amount wrong. Accepting payments that should have cured the default, then foreclosing anyway. CFPB regulations specifically prohibit servicers from advancing a foreclosure while evaluating you for loss mitigation if you applied more than 37 days before the sale.

A Boston-area homeowner won a wrongful foreclosure case after her servicer started foreclosure proceedings during the modification review period. The court didn't just stop the foreclosure—she got damages covering attorney fees plus compensation for the stress of fighting an improper proceeding. The servicer had to restart her modification review from scratch.

State laws pile on additional requirements. Some states mandate pre-foreclosure mediation. Others require specific waiting periods between default notice and sale. Many dictate exact language that must appear in notices. Skip these steps? The foreclosure might be void.

Documentation Requirements and Burden of Proof

The burden is on the lender to prove they have the legal right to foreclose. Many homeowners don't realize that challenging standing—especially in cases involving multiple loan transfers—can be one of the most effective foreclosure defense strategies

— Sarah Chen

In court foreclosures, lenders must prove their case—the whole thing. They need to establish ownership of the debt, your default, compliance with every notice requirement, and their legal right to foreclose. Just filing paperwork doesn't cut it.

Demand complete documentation: the original promissory note, the recorded mortgage, every assignment in the chain, your complete payment history, and proof they sent all required notices. Federal servicing rules require them to provide much of this on request. Discovery rules in litigation compel the rest.

Then examine what they produce with a critical eye. Affidavits signed by "robo-signers" who couldn't possibly have personal knowledge of your account? Payment histories showing mystery fees or payments applied to the wrong month? Assignments notarized in states where the signer wasn't physically present? These problems can unravel their case.

Alternatives to Foreclosure Defense in Court

Not everyone wants to wage a court battle. Several paths can resolve foreclosure without litigation—each carries different costs and benefits.

Alternative

How Long It Takes

Effect on Credit

Keep the House?

Works Best When

Loan Modification

Two to four months

Damages credit but far less than foreclosure

Yes—with changed loan terms

Your income can handle a reduced payment

Foreclosure Mediation

One to three months

Outcome-dependent

Maybe—if you reach agreement

Your state runs a formal program and you're willing to negotiate

Reinstatement

Right away to one month

Minor impact if done quickly

Yes—original loan continues

You've got cash to pay all arrears in one shot

Short Sale

Three to six months

Substantial damage but beats foreclosure

No

You can't afford the home long-term anyway

Deed-in-Lieu

One to three months

Similar credit hit as foreclosure

No

You want out fast without going through sale process

Loan Modification vs Foreclosure: Comparing Outcomes and Timelines

A loan modification rewrites your existing mortgage to make the payment something you can actually handle. How? The servicer might cut your interest rate, stretch the loan from 30 to 40 years, roll missed payments into the principal, or—rarely—reduce the principal itself.

You'll submit an application with pay stubs, bank statements, tax returns, a hardship letter explaining what went wrong, and detailed financial statements. Servicers must acknowledge receipt within 30 days. They've got 120 days to decide if you submitted everything at least 120 days before a scheduled sale.

Why modify beats foreclosure: you keep your home and avoid catastrophic credit damage. Sure, your credit report will show those past delinquencies. But completing a trial modification and getting current prevents the 200-to-300-point credit score nosedive that foreclosure causes.

The foreclosure alternative? Losing your house, credit destruction lasting seven to ten years, possible deficiency judgments (in states that allow them), and the chaos of forced relocation. For homeowners who can swing a modified payment, this isn't a close call.

Author: Olivia Carringt;

Source: redmonpestmgt.com

The catch: servicers reject applications constantly, sometimes for questionable reasons. "Incomplete documentation" (even when you sent everything). Income calculations that don't match their proprietary formulas. Investor restrictions buried in the securitization documents. You can appeal denials, but the process tests your patience.

The Foreclosure Mediation Process and How It Works

About 25 states and various localities offer foreclosure mediation—a sit-down between you, the lender's representative, and a neutral mediator exploring alternatives. Some jurisdictions make it mandatory; others require you to request it.

Mediation happens after foreclosure begins but before the sale. You'll get notice explaining your right to request mediation, usually with a 20-to-30-day response window. Request it, and the foreclosure pauses while mediation proceeds.

Good faith participation is required from both sides. Lenders must send someone with actual authority to make deals and bring complete loan files. You need to provide current financial documentation and income proof. The mediator guides the conversation but can't force either side to accept anything.

Successful mediations produce loan modifications, repayment plans, or short sale agreements. Even unsuccessful mediations deliver value—they delay foreclosure and often expose documentation problems you can use as defenses.

One New Jersey homeowner used court-ordered mediation to discover her servicer had charged her for an escrow shortage twice—once in the monthly payment, once as a separate fee. The mediator spotted the error during the document review. The servicer fixed the account, and the court dismissed the foreclosure. That outcome might never have emerged without mediation forcing both sides to review the numbers together.

Foreclosure Reinstatement: Paying Arrears to Stop the Sale

During the reinstatement period, you can stop foreclosure by paying everything past due—missed principal and interest, late fees, property inspections, attorney fees, foreclosure costs, the whole tab. Pay it, and your loan snaps back to the original terms like the default never happened.

State law determines your reinstatement rights. Some states grant a statutory right lasting until the auction gavel falls. Others limit it to specific windows—maybe 90 days from initial notice. Your loan documents might provide reinstatement rights exceeding state minimums.

Reinstatement makes sense after temporary hardship: you lost your job but found a new one, faced a medical emergency but recovered, dealt with a one-time crisis but your income's stable again. It works poorly if the original payment was already crushing you or if arrears have snowballed beyond any realistic lump sum.

Get the exact reinstatement figure in writing from your servicer—request a payoff statement. This number changes daily as interest compounds and fees accumulate. Pay by certified check or wire transfer so you've got documentation the payment cleared.

Critical Foreclosure Timeline Questions

When Is It Too Late to Stop Foreclosure in Your State

The point of no return depends on your state's system and foreclosure type. Judicial foreclosure states typically let you raise defenses until the court enters final judgment. Even post-judgment, some states provide redemption windows before the sale.

Non-judicial states compress everything. Once the notice of sale hits public records and newspapers, stopping it requires curing the default, filing bankruptcy, or getting a temporary restraining order based on legal violations. These options evaporate the moment the auctioneer says "sold."

Specifics matter. California, a non-judicial state, allows reinstatement until five business days before sale. After that? Only bankruptcy or a court order works. Florida, a judicial state, lets you contest until final judgment—typically 4-6 months post-filing if you don't respond, or 12-18 months if you fight.

The practical deadline arrives earlier than the legal one. Mounting effective defense takes time—gathering documents, consulting attorneys, filing proper responses. Waiting until days before sale leaves only emergency bankruptcy as an option.

Understanding Notice Periods and Response Deadlines

Foreclosure starts with notice. Judicial foreclosures begin with a summons and complaint giving you 20-30 days to file an answer (exact period varies by state). Miss it? The lender gets a default judgment without hearing your defenses.

Non-judicial foreclosures start with a notice of default or breach letter. State law dictates required content and your cure period—commonly 30 to 120 days. A subsequent notice of sale must be sent and published, typically 20-45 days pre-auction.

These deadlines don't bend. Courts rarely grant extensions. Servicers won't delay sales without court orders or bankruptcy filings. Calendar every deadline. Set phone reminders. If you're three days out and haven't acted, drop everything else.

Common mistake: assuming multiple notices mean more time. Each notice serves a distinct purpose with its own deadline. The default notice starts one clock. The sale notice starts another. Both matter independently.

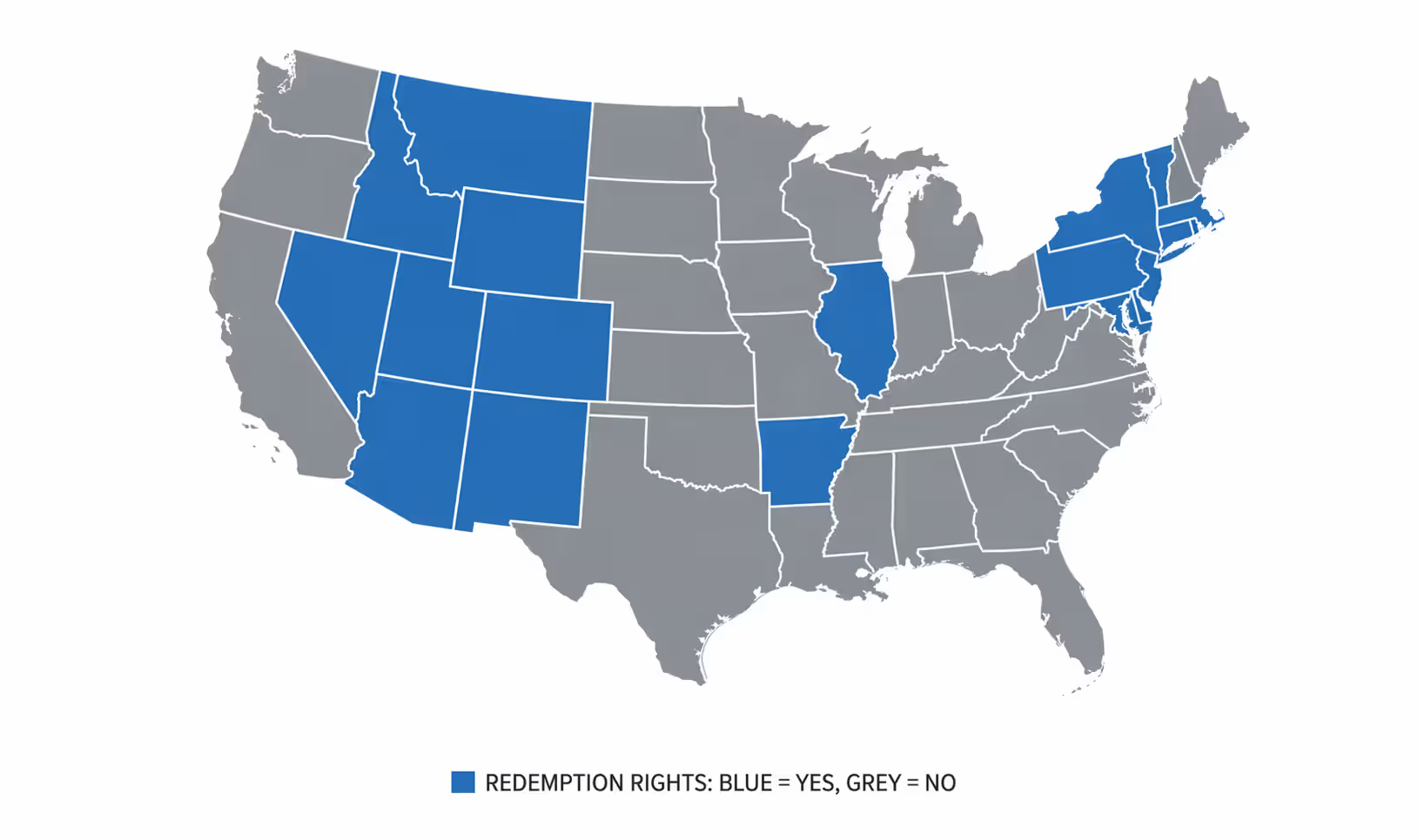

Statutory Redemption After Foreclosure: Post-Sale Recovery Rights

Statutory redemption lets former owners reclaim property after the foreclosure sale by paying the sale price plus costs and interest. About half of U.S. states provide this right, though terms vary dramatically.

Redemption periods run from 10 days to two years depending on state law, property type, and sale circumstances. Michigan gives six months for most properties, sometimes extending to twelve. Alabama provides one year. Georgia? Zero—sales are final immediately.

Redemption requires paying the full auction price, not your original debt. If an investor bought your property for $200,000, you need $200,000 plus interest and costs—even if you only owed $150,000. This makes redemption impractical for most homeowners who already couldn't afford the mortgage.

Some states grant occupancy rights during redemption. You can stay in the property during this period, though you might owe rent or use-and-occupancy charges. This creates breathing room to arrange financing, negotiate with the buyer, or prepare for moving.

Redemption rights are technical and unforgiving. Miss the deadline by 24 hours and it's gone. Some states require filing formal notice of redemption intent. Others require depositing funds with the court. Botch the procedure and you lose the right even with cash in hand.

State-by-State Variation in Redemption Periods

State laws create a redemption rights patchwork. Judicial states more commonly offer redemption than non-judicial ones, though plenty of exceptions exist.

No redemption states: California, Oregon, Washington, Virginia, Tennessee, Georgia. Foreclosure sales here are final—former owners have zero post-sale recovery rights.

Redemption states: Michigan (6-12 months), Alabama (one year), Iowa (varies by circumstances), North Dakota (60 days to one year), Wisconsin (six months to one year).

Some states attach conditions. If the sale price exceeds a certain percentage of assessed value, redemption might shorten or vanish. Abandoned properties sometimes lose redemption rights.

Before counting on redemption, verify current law in your specific state. Legislation changes. Court interpretations shift. Don't rely on online information without confirming it applies to your situation—consult a local attorney.

Author: Olivia Carringt;

Source: redmonpestmgt.com

Common Foreclosure Defense Mistakes to Avoid

Homeowners facing foreclosure often sabotage their own defense through preventable errors. Recognizing these traps improves your odds.

Ignoring notices and blowing deadlines causes the most damage. Every foreclosure notice requires action by a specific date. Miss the answer deadline on a foreclosure complaint? The lender gets a default judgment without hearing your defenses—even bulletproof ones become worthless if you don't raise them timely.

Fighting without documentation handicaps your case from the start. Challenging standing requires examining the title chain. Claiming predatory lending requires comparing disclosures to actual loan terms. Disputing the amount owed requires analyzing payment histories. Collect everything: the original note and mortgage, all servicer correspondence, payment records, modification applications, every notice received.

Misunderstanding bankruptcy's automatic stay creates false expectations. Yes, filing bankruptcy immediately stops foreclosure. But lenders can request relief from the stay—courts often grant it if you can't propose a viable plan. Chapter 7 gives temporary relief without curing arrears. Chapter 13 lets you catch up over 3-5 years but requires income sufficient for plan payments plus current mortgage. Filing bankruptcy without strategy wastes your protection.

Foreclosure rescue scams prey on desperate homeowners. Scammers promise to stop foreclosure for large upfront fees, then vanish. Others convince homeowners to temporarily deed property to them "for protection," then refuse to return it. Legitimate help comes from licensed attorneys, HUD-approved housing counselors, or legal aid organizations—none charge thousands upfront before delivering services.

Another trap: paying for unnecessary services. Some outfits charge $3,000+ for "forensic loan audits" supposedly uncovering legal violations. While loan document review has value, you can often get this through legal aid or as part of attorney representation. Standalone audits rarely justify their cost.

Failing to explore every option limits your outcomes. Some homeowners fixate on keeping the house regardless of financial reality. Others assume foreclosure is inevitable without investigating defenses. The smart approach evaluates everything—fighting foreclosure, modification, short sale, deed-in-lieu, even strategic default—based on your specific finances and goals.

Working with Foreclosure Defense Attorneys

Legal representation dramatically improves foreclosure defense outcomes, but timing and selection matter.

When to Hire Legal Help vs. Self-Representation

Complex cases demand attorney involvement. Challenging standing? Asserting predatory lending claims? Identifying wrongful foreclosure? You need someone who understands foreclosure law, civil procedure, and evidence rules. These defenses require legal research, document analysis, and courtroom advocacy beyond most homeowners' skills.

Simple situations might not need full representation. Applying for loan modification or pursuing mediation? A HUD-approved housing counselor provides guidance at no charge. If your state offers mediation and you're comfortable negotiating, you might handle it yourself with counselor support.

Middle ground option: limited scope representation. Some attorneys offer "unbundled" services—handling specific tasks like reviewing documents, drafting your complaint answer, or representing you at critical hearings while you manage other aspects. This cuts costs while ensuring professional help for technical parts.

You need an attorney when: you've been served with a foreclosure complaint, the sale date is approaching fast, you've spotted potential legal violations, the lender rejected your modification without clear justification, or you're considering bankruptcy.

What to Bring to Your First Consultation

Maximize your initial attorney meeting by bringing complete information. Attorneys can't evaluate your case without seeing relevant documents and understanding your situation.

Critical documents: promissory note, mortgage or deed of trust, all assignments and transfers, foreclosure complaint or default notice, lender and servicer correspondence, payment histories, modification applications and responses, current financial information showing income and expenses.

Create a timeline: when you got the loan, first missed payment, what caused the financial hardship, servicer communications, actions you've taken to resolve things.

Be honest about goals and financial reality. Can't afford the house even with modification? Say so. Want to delay foreclosure to save relocation money? Explain that. Attorneys can't help without understanding what you actually need.

Cost Structures and Legal Aid Options

Foreclosure defense attorneys typically charge hourly, flat fees, or hybrid arrangements. Hourly rates run $200-$500 depending on location and experience. Flat fees for specific services—filing an answer and initial motions—might cost $1,500-$3,500. Full representation through trial can hit $5,000-$15,000 or more.

Some attorneys take wrongful foreclosure claims on contingency when damages are involved. Win, and the attorney gets a percentage of recovery (typically 33-40%). Lose, and you owe nothing beyond costs. This only works when you've got strong monetary damage claims, not pure defensive strategies.

Legal aid organizations provide free representation to low-income homeowners. Eligibility typically requires income below 125-200% of federal poverty guidelines. Services may be limited to specific case types or defenses. Apply early—legal aid groups have limited capacity and often run waiting lists.

Bar associations in many states offer lawyer referral services and reduced-fee programs. Some law schools operate foreclosure defense clinics where supervised students provide free or low-cost assistance.

Red Flags When Choosing Representation

Not all attorneys are equally qualified or ethical. Watch for warnings: guaranteeing specific outcomes (honest attorneys can't guarantee wins), requesting massive upfront retainers without explaining what work it covers, or discouraging second opinions.

Verify credentials. Check your state bar to confirm the attorney is licensed and in good standing. Look for attorneys focusing on foreclosure defense or consumer law rather than general practitioners dabbling in occasional foreclosure cases.

Be wary of attorneys pushing bankruptcy as the only solution without exploring alternatives, or recommending deed-in-lieu or short sale without analyzing whether you've got valid defenses. The right attorney explores all options and helps you make informed decisions.

Communication counts. If an attorney doesn't return calls, can't explain legal concepts understandably, or makes you feel rushed or dismissed, find someone else. Foreclosure defense requires attorney-client collaboration.

Author: Olivia Carringt;

Source: redmonpestmgt.com

FAQ: Foreclosure Defense Strategies

Can I fight foreclosure if I'm behind on payments?

Absolutely. Being behind creates the default that triggers foreclosure, but it doesn't eliminate your right to challenge the process. Valid defenses—lack of standing, procedural violations, predatory lending—exist whether you're current or not. Courts evaluate the lender's right to foreclose separately from whether you owe money. That said, if you're just delaying the inevitable without a plan to cure default or transition out, you're extending stress without changing outcomes.

What is the strongest defense against foreclosure?

Challenging standing to foreclose typically packs the most punch because it questions whether the foreclosing entity has any right to foreclose at all. If the lender can't prove continuous ownership from original lender to current note holder, courts must dismiss the foreclosure. This works regardless of whether you owe money—the question is whether this particular plaintiff can collect through foreclosure. Predatory lending and wrongful foreclosure claims can be powerful too, but they require proving specific illegal conduct. Standing challenges exploit the lender's documentation gaps.

How long does foreclosure defense typically delay the process?

Delays vary wildly based on your state, defense strength, and lender response. Filing an answer in a judicial state typically adds 6-12 months as the case moves through discovery and potential trial. Requesting mediation might add 60-90 days. Bankruptcy creates an immediate stay lasting months in Chapter 7 or years in Chapter 13. Asserting weak defenses without evidence might delay things only 30-60 days before the court grants summary judgment. The real question isn't delay length, but whether you're using that time productively to pursue modification, arrange financing, or prepare for transition.

Does filing bankruptcy stop foreclosure immediately?

Yes—filing bankruptcy triggers an automatic stay halting foreclosure and most collection actions instantly. The stay takes effect the moment you file, even if the sale is scheduled for later that day. But the protection is temporary. In Chapter 7, the stay lasts until case conclusion (typically 3-4 months) unless the lender gets relief from stay, which courts often grant if you're not proposing a way to cure arrears. Chapter 13 provides stronger protection by letting you cure arrears over 3-5 years while maintaining current payments, but you need sufficient income to fund the plan. Filing without a viable plan wastes your protection.

Can I get my home back after a foreclosure sale?

In states with statutory redemption, yes—but it's difficult and expensive. You must pay the full sale price plus interest and costs within the redemption period (ranging from 10 days to 2 years depending on state). If an investor bought your home for $250,000, you need $250,000 plus costs regardless of your original loan balance. Most homeowners who couldn't afford the mortgage can't produce the redemption amount. In states without redemption (about half of U.S. states), the sale is final—you have no right to reclaim property. Your only option would be negotiating with the new owner to repurchase, which they're not obligated to consider.

What documents do I need to challenge a foreclosure?

Start with loan documents: original promissory note, mortgage or deed of trust, all modifications or amendments. Obtain every assignment and transfer from the county recorder's office—these show ownership chain. Request complete payment history from your servicer showing every payment, fee, and charge. Gather all lender and servicer correspondence, including modification applications, denial letters, account statements. If you're in judicial foreclosure, get the court file including complaint, all affidavits, and supporting documents the lender filed. For predatory lending claims, you need original loan disclosures, Good Faith Estimate, and communications from loan origination. The more complete your documentation, the better you can identify weaknesses in the lender's case.

Foreclosure defense strategies span from technical legal challenges to negotiated alternatives—each fits different circumstances and goals. Homeowners achieving the best outcomes start early, gather complete documentation, understand their options, and make strategic decisions based on financial reality rather than emotion.

Whether you challenge standing, negotiate modification, or pursue statutory redemption, success requires understanding your state's specific rules and your timeline. The foreclosure process moves quickly once it starts—options available today may disappear tomorrow.

Facing foreclosure? Act now. Consult a HUD-approved housing counselor. Review loan documents for potential defenses. Consider whether legal representation makes sense for your situation. Even if you ultimately can't save your home, proper defense buys time to prepare for transition, potentially reduces or eliminates deficiency liability, and ensures the lender follows proper procedures.

The worst strategy? No strategy—ignoring the problem and hoping it resolves itself. The second-worst? Pursuing defenses without understanding whether they're viable or how they serve your long-term interests. Educate yourself, get qualified help, and make informed decisions about your home and financial future.

A tax lien is a legal claim the government places against your property when you fail to pay taxes. Unlike a levy, which seizes assets, a lien secures the government's interest and can prevent you from selling or refinancing until resolved. Understanding the differences between federal, state, and property tax liens is essential

Foreclosure isn't inevitable. Homeowners who understand their options and act quickly can often save their homes or exit on better terms. Learn the timeline, your rights, and actionable strategies including government programs, bankruptcy protection, and alternative solutions

RESPA violations cost homebuyers thousands through hidden kickbacks and undisclosed arrangements. This guide explains prohibited practices like Section 8 kickbacks, disclosure failures, and unearned fees—plus the legal remedies available when lenders, title companies, or brokers violate federal law

Property owners overpay billions in taxes annually due to inflated assessments. Learn the complete process to challenge your property tax assessment, from filing deadlines and evidence gathering to informal reviews and formal ARB hearings, with strategies for both residential and commercial properties

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to real estate law, property rights, leases, liens, zoning, landlord-tenant disputes, and litigation.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal outcomes may vary depending on jurisdiction, property type, and individual circumstances.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified attorneys or real estate professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.