Imagine discovering you can't refinance your home because a contractor you paid three years ago filed a claim against your property. Or learning at closing that an old lawsuit resulted in a creditor's claim that must be settled before you can sell. These scenarios happen to thousands of homeowners because of property liens—legal instruments that give creditors a stake in your real estate's value.

A lien transforms an ordinary debt into a claim secured by your property. Unlike credit card debt or personal loans, these secured interests follow the property through ownership changes and can prevent sales, block refinancing, and even lead to forced auctions. Whether you're purchasing your first home, managing rental properties, or settling an estate, understanding these legal mechanisms protects you from financial complications that could derail your plans.

Understanding Property Liens

Think of a property lien as a legal safety net for creditors—it's their guarantee that they'll eventually get paid. More precisely, it's a recorded claim that encumbers real estate, securing repayment of money owed or fulfillment of an obligation.

Here's the fundamental mechanism: liens attach to the property itself rather than just the owner. This distinction matters enormously. If you owe money on a credit card, the debt follows you personally. But when someone places a lien on your home, that claim stays with the real estate. Sell the house to your cousin, and the lien remains—it becomes your cousin's problem unless you've cleared it first.

The process follows a standardized procedure. A creditor with a valid claim files specific documentation with your county's recording office. This filing creates public notice that your property now has an encumbrance. The creditor doesn't gain ownership rights, but they do acquire a secured position. Try to sell or refinance, and title examiners will discover this claim during their search, requiring resolution before the transaction can close.

The range of entities that can encumber your property extends far beyond banks. Mortgage companies obviously hold liens when you finance a purchase. Construction professionals—from general contractors to plumbers and electricians—can secure payment through mechanic's claims. Tax collectors at federal, state, and local levels impose liens for delinquent obligations. Your homeowners association can file claims for unpaid assessments. Someone who wins a court case against you can convert that judgment into a property encumbrance in any county where you own real estate.

These claims carry legal weight because state statutes authorize them and public recording systems make them enforceable. Once properly documented, lienholders gain specific remedies, often including foreclosure rights. The precise procedures and homeowner protections differ across state lines, but the core concept remains universal: secured creditors have carved out a position in your property's equity.

Author: Samantha Holloway;

Source: redmonpestmgt.com

Types of Property Liens

Property liens fall into distinct categories, each with different characteristics, priorities, and removal processes. Recognizing these differences helps you evaluate risk and understand your options.

Voluntary Liens

Consensual liens arise from agreements you actively enter. When you take out a home loan, you create this type of encumbrance by signing the mortgage documents. The same principle applies to home equity credit lines and second mortgages.

These arrangements are transparent—you know exactly what you're agreeing to because you've signed multiple pages of disclosures. You also understand the exit path: fulfill the payment schedule, and the lender executes a release. Because these liens typically get recorded at purchase or refinancing, they usually occupy the first priority position.

Voluntary liens represent a straightforward exchange: you receive financing, and in return, you grant the lender security in your property. Both parties understand the terms from the outset.

Involuntary Liens

Creditors impose these claims without requiring your approval, typically after you've failed to satisfy an obligation. Common examples include:

Mechanic's liens: These arise when construction professionals don't receive payment for work performed on your property. The complexity here can surprise homeowners: you might face a lien from someone you never contracted with directly. Perhaps your general contractor failed to pay the electrician—that electrician may still have the right to lien your property under state law, despite having no contract with you.

Judgment liens: After winning a lawsuit and obtaining a monetary judgment, creditors can transform that court order into a property encumbrance. They accomplish this by recording an abstract of judgment with the county recorder. This converts unsecured litigation debt into a claim secured by any real estate you own in that jurisdiction.

HOA liens: Homeowners associations secure unpaid fees, special assessments, and sometimes even fines through property liens. These claims can grow surprisingly fast when monthly dues compound with late fees and collection costs.

The defining characteristic of involuntary liens: they frequently appear without warning. You might discover a mechanic's lien only when you apply for refinancing, or learn about a judgment lien from a decades-old dispute you believed was settled.

Tax Liens and Government Claims

Government liens deserve focused attention because of their superior priority and aggressive enforcement mechanisms. When you fall behind on property taxes, the county automatically holds a secured claim—usually taking precedence over virtually every other debt, including mortgages recorded years earlier. Continued non-payment can result in a tax foreclosure sale where the county auctions your property to recover the delinquent amount.

The IRS creates federal tax liens when you owe income tax that remains unpaid after assessment. Following a specific administrative process, they file a Notice of Federal Tax Lien with your county recorder. This filing encumbers all property and rights to property you hold in that county. State revenue departments employ similar mechanisms for unpaid state income taxes.

Additional government claims include municipal liens for unpaid utilities (water, sewer, garbage in some areas) and code enforcement liens resulting from building violations. These can accumulate quietly while property owners remain unaware of the growing debt.

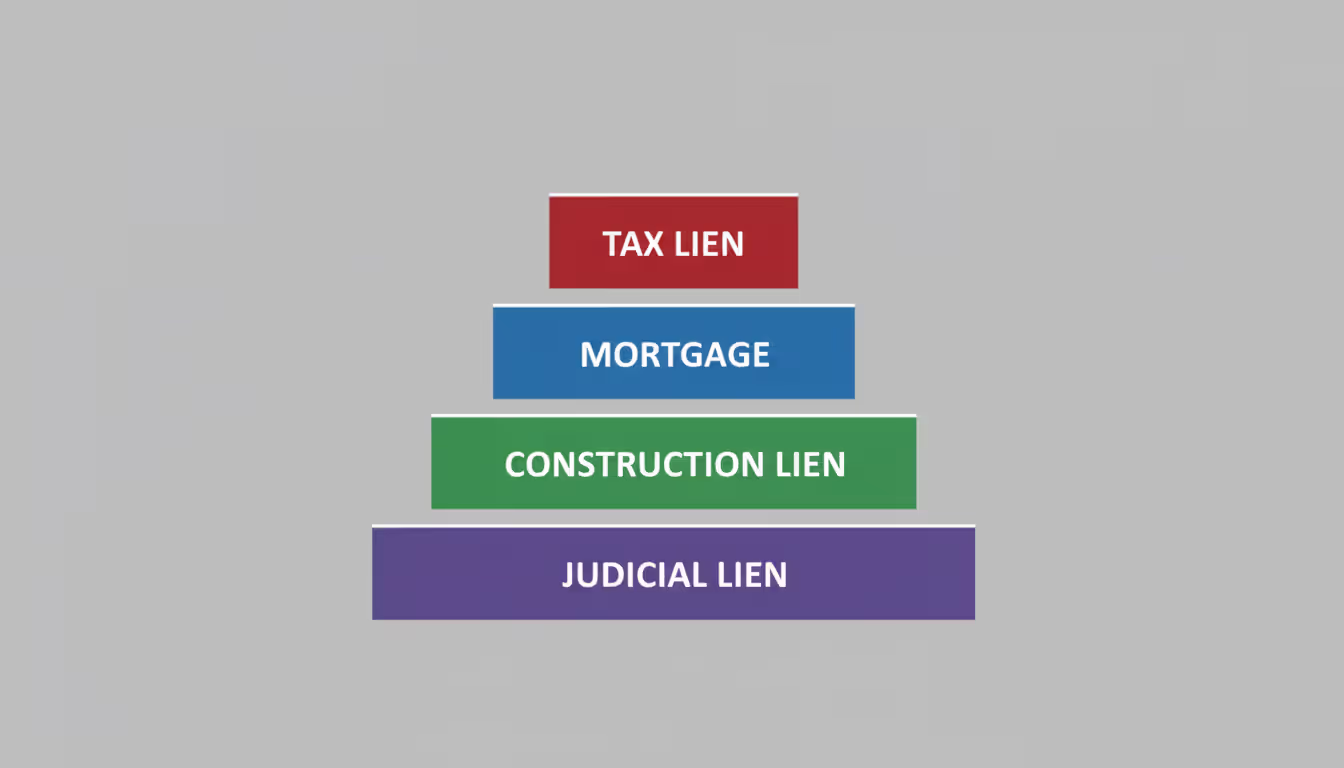

How Lien Priority Works

When several liens encumber the same property, priority determines the payment sequence if the property sells or goes through foreclosure. This ranking system becomes critical when sale proceeds fall short of total debt—creditors lower in priority may receive partial payment or nothing at all.

Recording date generally controls priority: the earliest-recorded lien holds first position, the next holds second, and so forth. Picture liens as a queue—first documented, first paid. When a property sells, the proceeds flow down this line in order.

Several significant exceptions disrupt the recording date rule:

Property tax liens jump to the front of the line regardless of recording date. A tax lien filed this month takes priority over a mortgage recorded ten years ago. This super-priority protects municipalities' ability to fund essential services regardless of other claims on the property.

HOA liens receive limited super-priority in certain states, but courts typically cap this priority at six to twelve months of unpaid dues. Any amounts beyond this cap fall into the standard priority queue based on recording date.

Mechanic's liens can have retroactive priority in many jurisdictions. Even though recording occurs after work completion, the lien's priority may reach back to when construction commenced. This means a mechanic's lien could outrank a construction loan recorded after the project started.

Foreclosure eliminates subordinate liens (those ranked lower) but leaves superior liens (higher priority) intact. Consider this scenario: the holder of a second mortgage forecloses. The first mortgage survives, and the foreclosure buyer takes title subject to it. Conversely, when the first mortgage forecloses, the second mortgage gets wiped out.

Priority rules matter intensely for buyers considering foreclosed properties and homeowners negotiating with multiple creditors. A creditor in fourth position on a property worth less than the first mortgage debt knows foreclosure will yield them nothing, making them more receptive to settlement negotiations or discounted payoffs.

Author: Samantha Holloway;

Source: redmonpestmgt.com

How to Check If There's a Lien on Your Property

Discovering whether real estate carries liens means examining public records through several channels:

County recorder searches: Each county maintains official records of documents affecting real property within its boundaries. Access these by visiting the recorder's office during business hours or through their website if they've digitized records. You'll search using the property's street address or the assessor's parcel number. Look for mortgages, deeds of trust, abstracts of judgment, mechanic's claims, and tax liens. Many counties have converted decades of paper records to digital format, though historical documents sometimes require in-person research.

Professional title searches: The gold standard is hiring a title company to conduct a comprehensive examination. For fees ranging from $150 to $400, they'll scrutinize all relevant records and deliver a detailed report showing ownership history and every recorded encumbrance. Buyers routinely order these searches, and lenders typically require them before approving loans.

Online resources: Various states and counties provide free web portals for searching recorded documents. Commercial services compile public records into searchable databases, though they often require paid subscriptions. Remember that online resources sometimes contain gaps or lag behind current recordings, so verify critical information through official county sources.

Tax assessor records: Contact your county tax assessor to verify current tax status. Delinquent property taxes create automatic liens even without a separate recorded document.

HOA inquiries: For properties within homeowners associations, request a status letter directly from the association showing current standing on dues and assessments.

Federal tax lien searches: Look in the county recorder's grantor-grantee index under the property owner's name. IRS liens attach to all real and personal property owned by the taxpayer within that county.

When investigating your own property, begin with your county's online record system, searching both your name and the property address. Review your credit report for judgments (though liens don't always appear on credit files). Before listing your property for sale or applying for refinancing, invest in a professional title search to identify issues you might have overlooked.

Common mistake: assuming that because you didn't consent to something, it can't exist. Involuntary liens require no signature or permission. Judgment liens can be recorded in any county where you hold property, not necessarily where the court case was filed.

How Liens Affect Selling or Buying Property

Author: Samantha Holloway;

Source: redmonpestmgt.com

Liens introduce complications into real estate transactions because they prevent transfer of clear, marketable title. Purchasers want ownership free from claims that could jeopardize their investment. Lenders insist on clear title because their mortgage must hold first position to adequately secure the loan.

Selling property carrying liens typically requires paying them off at closing. The settlement agent includes these payoffs in the closing statement, deducting them from your sale proceeds. If your sale price fails to cover all liens plus closing costs, you'll either bring cash to the closing table or negotiate with creditors to accept reduced payments (known as a short sale for mortgage liens).

Most states mandate seller disclosure of known liens, though title examinations reveal recorded liens regardless of whether sellers disclose them. Failing to disclose a lien you're aware of can expose you to fraud liability.

Buyers receive protection through multiple safeguards. Title examinations uncover liens before closing occurs. Title insurance policies protect against liens that weren't discovered during the search process. Purchase agreements typically include contingencies requiring sellers to deliver clear title, giving buyers an escape route if liens can't be resolved satisfactorily.

One trap catches uninformed buyers: purchasing property at foreclosure or tax auctions. These sales often exclude title insurance, and buyers take title subject to certain liens depending on which creditor initiated the foreclosure. Someone buying at a junior lienholder's foreclosure might acquire property still burdened by senior liens.

Refinancing faces similar obstacles. Lenders demand clear title except for the liens they're creating or maintaining. When refinancing your first mortgage, junior lienholders must either subordinate (agree to maintain second position behind your new loan) or be paid off entirely.

Liens don't render property unsaleable, but they do complicate the process and reduce net proceeds. Buyers should never forgo title searches to save money—the modest cost pales in comparison to the risk of accepting title to encumbered property.

How to Remove a Lien from Your Property

Property owners make a critical error when they ignore liens, hoping the problem will somehow resolve itself.Any lien on your title creates an impediment that will absolutely block you from selling or refinancing until you deal with it properly. Even when you genuinely dispute the underlying debt, you must address the lien through appropriate legal procedures. I've watched real estate closings collapse one day before scheduled signing because sellers assumed an old mechanic's lien had expired on its own, when the creditor had actually renewed it. My advice: order a comprehensive title search well ahead of any planned closing, allowing sufficient time to resolve whatever issues emerge

— Jennifer Martinez

Clearing a lien requires either satisfying the obligation or demonstrating the claim lacks validity. Here are the principal approaches:

Satisfy the debt: The most direct path is paying what you owe. After payment, the lienholder must execute a lien release or satisfaction of lien, which you then record with the county to clear public records. Mortgage lenders usually handle recording the release automatically. For other lien types, you may need to verify that recording happens—don't assume it occurs without follow-up.

Settlement negotiations: When full payment isn't feasible, negotiate with the lienholder for a reduced amount. They may accept less than the full debt, particularly if they hold junior position and would collect nothing through foreclosure. Obtain written settlement agreements before submitting payment, ensuring they explicitly require the lienholder to release the claim.

Challenge invalid liens: If a lien was improperly filed or the underlying debt lacks merit, you can contest it. Mechanic's liens carry strict filing deadlines and procedural requirements; claims filed beyond the statutory window or without proper notice can be attacked. File a motion asking the court to release or expunge the lien, presenting evidence of its invalidity. The lienholder must then substantiate their claim or the court orders removal.

Allow expiration: Certain liens expire automatically after set periods. Judgment liens typically expire after five to twenty years depending on state law, unless the creditor renews them. Mechanic's liens expire if the lienholder doesn't initiate foreclosure within the statutory deadline (commonly ninety days to one year following recording). Federal tax liens expire ten years after assessment if the IRS takes no collection action. Relying on expiration carries risk since creditors can often extend their claims.

Post a bond: In specific situations, you can post a surety bond to release the property while disputing the debt. This frequently occurs with mechanic's liens. You pay a bonding company to issue a bond covering the lien amount, transferring the claim from your property to the bond. This enables you to sell or refinance while the underlying dispute continues.

Bankruptcy options: Filing bankruptcy can eliminate certain lien types. Judgment liens can often be avoided (removed) in bankruptcy when they impair exemptions you're entitled to claim. However, consensual liens like mortgages and particular statutory liens like tax claims survive bankruptcy.

Documentation is essential for lien removal. Maintain payment proof, secure written releases, and record those releases promptly. If a lienholder refuses to release a satisfied lien, file a lawsuit to compel release—you may recover damages for wrongful refusal.

Comparison of Common Lien Types

Lien Type

Consensual or Non-Consensual

Standard Priority

Creation Process

Removal Method

Mortgage Lien

Consensual

First position when recorded at purchase

Borrower signs loan documents; lender records mortgage or deed of trust

Satisfy loan terms; lender files release of lien

Mechanic's Lien

Non-consensual

Varies by state; may have retroactive priority to construction commencement

Construction professional files claim within statutory deadline after non-payment

Pay debt and obtain release, or successfully dispute claim validity

Property Tax Lien

Non-consensual

Super-priority status; supersedes all other claims

Arises automatically when property taxes become delinquent

Pay overdue taxes plus accumulated interest and penalties

Judgment Lien

Non-consensual

Determined by recording date

Prevailing party records abstract of judgment with county

Satisfy judgment, negotiate settlement, or wait for statutory expiration

HOA Lien

Non-consensual

Limited super-priority in certain states

Association records lien for unpaid dues, assessments, or fines

Pay outstanding balance and obtain written release from association

Frequently Asked Questions About Property Liens

Can I sell my house if there's a lien on it?

Yes, selling remains possible, but the lien typically must be satisfied at closing using sale proceeds. Title companies insist on releasing the lien before they'll transfer clear ownership to your buyer. When your sale price fails to cover all liens plus closing expenses, you'll need to contribute additional cash at closing or negotiate with creditors to accept reduced settlements.

How long does a lien stay on your property?

Duration depends on lien type and applicable state law. Mortgage liens remain attached until you repay the loan completely. Judgment liens generally persist for five to twenty years but creditors can renew them in most states. Mechanic's liens expire when the lienholder fails to initiate foreclosure within ninety days to two years after filing, depending on jurisdiction. Property tax liens continue until you pay the taxes and can trigger foreclosure sales within several years. Federal tax liens last ten years from the assessment date but can be refiled.

Does a lien affect my credit score?

Impact varies by lien type. Mortgage liens don't harm credit when you maintain timely payments—they're expected obligations. Tax liens and judgment liens may appear on credit reports and damage scores, though tax lien reporting has diminished since 2018 policy changes. The underlying debt that triggered the lien (unpaid invoices, court judgments) definitely impacts credit. Even liens absent from credit reports can prevent new credit approvals because lenders discover them during title examinations.

What happens to liens when the property owner dies?

Liens continue to encumber the property after the owner's death. When property transfers through probate or trust administration, the estate must resolve liens before distributing assets to beneficiaries. Heirs who inherit real estate receive it subject to existing liens. If the estate sells the property, lien satisfaction comes from sale proceeds. If heirs retain the property, they must either pay liens off or continue payments on consensual liens like mortgages. Certain liens, including federal tax liens for the deceased's income tax debts, attach to all estate assets.

Can a lien be placed on my property without my knowledge?

Yes, creditors routinely record involuntary liens without property owners' direct awareness. After winning lawsuits, judgment creditors can record liens even when you didn't respond to the case or realize it was filed. Contractors can file mechanic's liens when payment disputes arise. The IRS can record tax liens without seeking permission. However, most lien types require some notice form, even if you don't receive personal notification. Mechanic's liens mandate preliminary notices in most jurisdictions. Judgment liens require lawsuit service. Tax liens follow administrative assessment procedures. The recording itself provides constructive notice to everyone, including property owners.

How much does it cost to remove a lien?

The primary expense is satisfying the underlying obligation—paying what you owe plus accumulated interest and penalties. Recording a release document typically costs $15 to $50 in county fees. Hiring an attorney to negotiate settlements or contest invalid liens can range from $500 to several thousand dollars depending on case complexity. Title companies charge $150 to $400 for searches identifying liens. Bonding around a lien costs approximately 1% to 3% of the lien amount annually in bond premiums. Some states permit lienholders to add their attorney fees and collection costs to the lien amount, increasing your required payment.

Property liens represent one of real estate ownership's most significant aspects, yet they remain misunderstood until they create immediate problems. Whether you're managing a consensual lien you agreed to, confronting an involuntary lien that surprised you, or verifying that property you're purchasing carries no encumbrances, the solution is proactive management rather than reactive crisis response.

Begin by knowing your title status. Current property owners should order title searches every few years to detect liens recorded without their knowledge. Before purchasing property, never eliminate the title search to reduce costs—the minimal expense provides insurance against inheriting another party's debt complications. Upon discovering a lien, avoid both panic and procrastination. Most liens can be resolved through payment, negotiation, or legal challenge when they lack validity.

The public recording system provides transparency and protects creditor rights while simultaneously working in your favor. Because liens appear in public records, you can discover them before they disrupt transactions. Because releases also get recorded, you can document that liens have been satisfied. Understanding lien mechanics, priority rules, and removal procedures equips you to protect your property rights and navigate real estate transactions successfully.

Whether you own property, plan to purchase, or invest in real estate, treating lien searches and resolution as standard ownership practices will prevent expensive surprises and keep your transactions moving forward smoothly.

A tax lien is a legal claim the government places against your property when you fail to pay taxes. Unlike a levy, which seizes assets, a lien secures the government's interest and can prevent you from selling or refinancing until resolved. Understanding the differences between federal, state, and property tax liens is essential

Foreclosure isn't inevitable. Homeowners who understand their options and act quickly can often save their homes or exit on better terms. Learn the timeline, your rights, and actionable strategies including government programs, bankruptcy protection, and alternative solutions

RESPA violations cost homebuyers thousands through hidden kickbacks and undisclosed arrangements. This guide explains prohibited practices like Section 8 kickbacks, disclosure failures, and unearned fees—plus the legal remedies available when lenders, title companies, or brokers violate federal law

Property owners overpay billions in taxes annually due to inflated assessments. Learn the complete process to challenge your property tax assessment, from filing deadlines and evidence gathering to informal reviews and formal ARB hearings, with strategies for both residential and commercial properties

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to real estate law, property rights, leases, liens, zoning, landlord-tenant disputes, and litigation.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal outcomes may vary depending on jurisdiction, property type, and individual circumstances.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified attorneys or real estate professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.