Here's something most property buyers don't realize: when you buy land, you're not just getting the dirt. You're getting a whole package of rights—including the sky above your building.

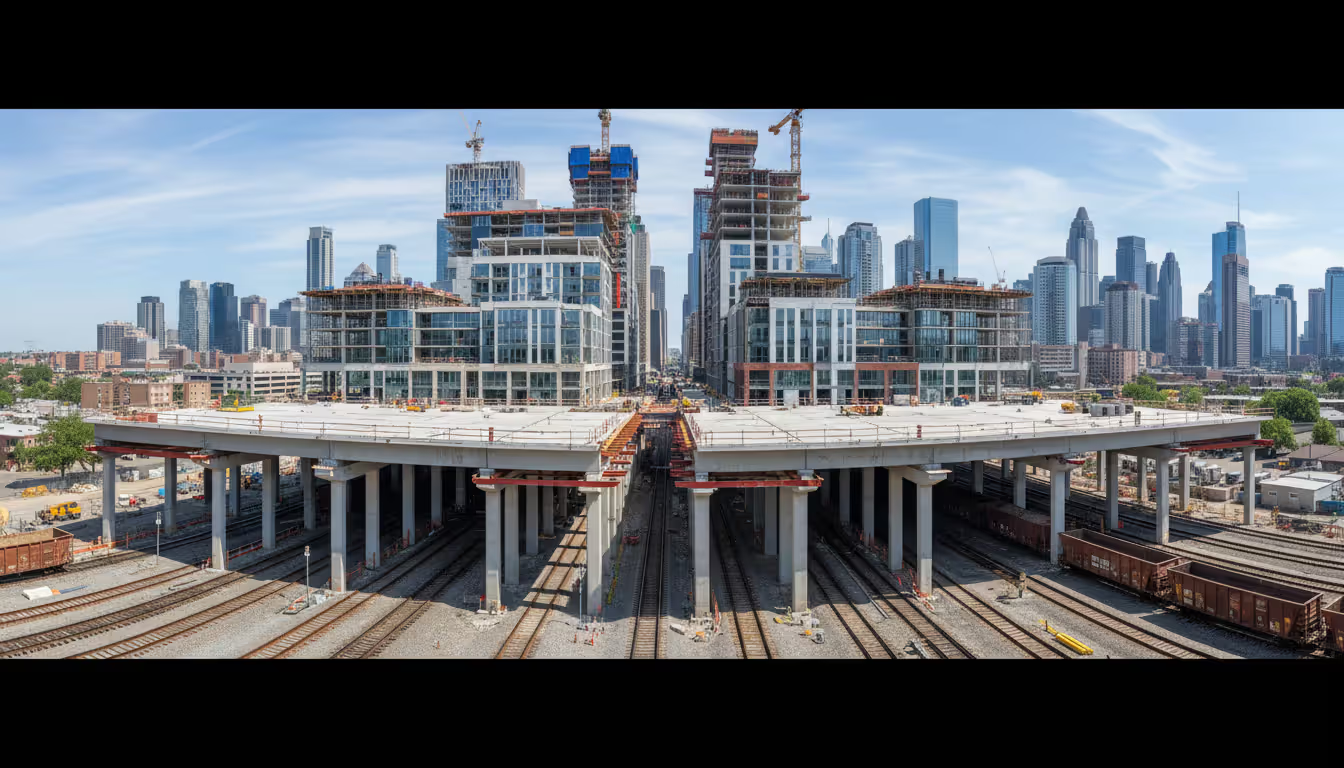

Think about it. A developer in Manhattan pays millions for a skinny lot between two skyscrapers. The land itself? Maybe 2,000 square feet. But the vertical space stretching 50 stories up? That's where the real value lives. That vertical space—those are air rights, and they've become one of the hottest commodities in urban real estate.

Here's why this matters: A church sitting on valuable downtown real estate might never want to tear down their 100-year-old building. But they can sell the unused space above it to a neighboring developer for $8 million. The church stays put, gets a financial windfall, and the developer builds three extra floors on their adjacent tower. Everyone wins.

This gets complicated fast, though. Air rights interact with zoning codes, can be split off from the land itself, and work completely differently than mineral rights or water rights. Let's break down exactly how this works.

Air Rights Definition and Legal Framework

Air rights definition: The ownership interest in vertical space above a piece of land, giving you the ability to build upward, sell that building capacity to someone else, or lease it out—all within whatever limits your local zoning allows.

There's an old property law concept, originally in Latin (cuius est solum), that roughly translates to "own the land, own everything from the center of the earth to the heavens." Medieval stuff. Obviously that's not how it works anymore—airlines would have a rough time if they needed permission from every property owner below their flight path.

Modern reality? You own the airspace directly above your property up to a point. The FAA sets the ceiling where navigable airspace begins (usually around 500 feet in cities, higher in rural areas). Below that threshold, local governments control what you can build through zoning.

What are air rights in real estate deals? Here's the practical version: Let's say zoning allows 20-story buildings in your area. You own a 5-story building. You've got 15 stories of unused development rights sitting there. In the right market, those 15 stories are worth real money—even if you never plan to build them yourself.

The Supreme Court settled the big legal question back in 1978 with Penn Central Transportation Co. v. New York City. Penn Central wanted to build a tower on top of Grand Central Terminal. The city's landmarks commission said no. Penn Central sued, arguing this was an unconstitutional taking of their property rights.

The Court ruled that New York could restrict development on landmarks, but had to provide a way for owners to recapture value—specifically through transferable development rights. This decision created the legal framework for modern air rights markets in dozens of cities.

Author: Daniel Crosswell;

Source: redmonpestmgt.com

Zoning shapes everything here. Your air rights are only worth what zoning permits. A property in a single-family neighborhood might have 30 feet of unused vertical space, but if zoning caps buildings at 35 feet and you're already at 32 feet, you've got 3 feet to work with. Compare that to a Midtown Manhattan lot where zoning allows 600 feet and you're at 200 feet—now you're sitting on a gold mine.

How Air Rights Work in Practice

Cities measure development capacity using floor area ratio, or FAR. It's simpler than it sounds. FAR compares total building square footage to lot size.

Example: 10,000-square-foot lot, FAR of 8.0. You can build 80,000 square feet of floor space total. Maybe that's 8 floors of 10,000 square feet each. Maybe it's 40 floors of 2,000 square feet each. The FAR doesn't care about the shape—just the total.

Now say you only build 30,000 square feet on that lot. You've got 50,000 square feet of unused FAR. That's your sellable air rights, assuming your city allows transfers.

Cities calculate this differently. Some exclude mechanical space, parking, or basements from FAR. Others count every square inch. New York has one set of rules. Chicago uses different ones. You need local expertise to figure out exactly what you've got.

Air Rights in Urban Development

Dense cities treat air rights like any other commodity. Supply and demand.

Take Manhattan's Midtown. Air rights traded at $300 per buildable square foot in 2024. A synagogue with a modest building on a 4,000-square-foot lot might have 30,000 unused square feet. Quick math: that's $9 million sitting above their roof.

The synagogue doesn't want to move. A developer next door needs more height for a luxury condo tower to pencil out financially. They buy the air rights, cantilever their building over the synagogue's property line (with easements and structural agreements), and build 10 extra floors. The synagogue gets $9 million for renovations and programs. The developer unlocks a project that generates $50 million in additional revenue.

This happens constantly in cities with land scarcity:

Developers assemble air rights from 5-6 neighboring properties to create a massive tower on a small footprint

Railroads owning linear rights-of-way sell millions of square feet to projects built above their tracks

Historic theaters and churches become unexpected revenue generators

Property owners who bought decades ago discover their biggest asset isn't the building—it's the unused space above it

Author: Daniel Crosswell;

Source: redmonpestmgt.com

Zoning and Height Restrictions

Here's where it gets tricky. FAR limits are one thing. Absolute height limits are another.

Your property might have unused FAR, but if there's a 200-foot height cap and you're already at 180 feet, you've got 20 feet to work with—regardless of how much FAR you have left. Both constraints matter.

Zoning can include: - Absolute height maximums (common near airports) - View corridor protections (preserving sight lines to landmarks) - Setback requirements that force upper floors to step back from the street - Shadow regulations (yes, really—some cities limit how much shadow new buildings can cast on parks) - Historic district overlays that trump underlying zoning

Cities sometimes use contextual zoning where permitted heights decrease as you move away from commercial cores. A downtown parcel might allow 800 feet. Three blocks east? 350 feet. Six blocks east? 150 feet. Air rights don't transfer across these boundaries—they're geographically locked.

Smart developers study comprehensive plan updates and rezoning proposals. A property currently zoned for 10 stories might jump to 25 stories if the city upzones the neighborhood. Buy air rights before that happens, and you've just captured enormous value.

Selling and Transferring Air Rights

Cities with formal transferable development rights programs make this process structured. Cities without them? Transactions happen anyway, but only between adjacent properties and with more legal complexity.

TDR programs work like this: City identifies "sending zones" (historic districts, open space, farmland they want preserved) and "receiving zones" (growth areas where they want development concentrated). Property owners in sending zones can sell development rights they can't use. Developers in receiving zones buy those rights to build bigger than their lot alone would allow.

Air rights transactions have evolved from novelty deals to mainstream development tools. The challenge isn't whether these rights can be monetized—it's structuring transactions that satisfy both sophisticated buyers seeking certainty and sellers who may be unfamiliar with the intricacies of development finance

— Sarah Mitchell

Here's how a typical transaction unfolds:

Step 1: Title and zoning analysis. You need to confirm the sending property actually has transferable rights. Some buildings used bonus FAR provisions that aren't transferable. Others already sold their air rights in 1987 and nobody recorded it properly. Get a surveyor and zoning attorney involved early.

Step 2: Valuation. Three methods get used: - Comparable sales: What did similar air rights sell for in the past 12 months within three blocks? - Residual method: Developer works backward from project pro forma—what can they pay for air rights while still hitting their required return? - Income approach: What's the net present value of additional rental income from extra floors?

These methods can give wildly different answers. A seller might think their rights are worth $400/sf based on comparable sales. A buyer's residual analysis might show they can only pay $220/sf. Negotiation bridges that gap.

Step 3: Municipal approvals. Most TDR programs require certification. The city confirms the sending site has the rights, verifies the receiving site can legally accept them, and approves the transfer. This isn't rubber-stamping—expect 60-120 days and potential pushback from community boards.

Step 4: Permanent restriction. The sending site gets a recorded easement or deed restriction preventing future development. This runs with the land forever. Future owners can't come back and try to develop what you already sold.

Step 5: Closing and recording. Development rights certificates get issued (if your city uses those), deeds are executed, and everything gets recorded in public records. Buyers usually want title insurance covering the air rights transfer.

Who's buying? Primarily developers with active projects. They need the rights now to finalize plans. Occasionally you'll see speculative investors buying in hot neighborhoods, betting that demand increases before they sell. Family offices sometimes acquire air rights as alternative investments with low correlation to traditional real estate.

Sellers include religious institutions (churches, synagogues, mosques with beautiful buildings they want to preserve), cultural organizations (theaters, museums), railroads (sitting on massive linear holdings), parking lot owners (happy with steady parking revenue, no desire to develop), and elderly property owners (content with small buildings, interested in liquidity).

Air Rights vs. Other Property Rights

Property ownership splits into distinct pieces that can be separated and sold independently. Here's how they compare:

Property Right Type

What It Includes

Can You Sell It Separately?

What's It Used For?

Who Usually Owns It?

How Do You Value It?

Air Rights

Vertical space from ground level up to FAA limits

Yes, in cities with TDR programs; otherwise typically only to adjacent parcels

Building taller structures, billboards, infrastructure passing overhead

Surface owner unless previously severed

Multiply unused FAR by $/sf based on comparable sales or residual value analysis

Mineral Rights

Oil, gas, coal, metals, and other subsurface resources

Yes, freely transferable; frequently separated from surface in energy states

Resource extraction, royalty income from production

Often severed from surface; requires title search going back decades

Geological reports, commodity prices, royalty rates (typically 12.5%-25% of production)

Water Rights

Use of surface water or groundwater

Depends—riparian rights transfer with land; prior appropriation rights may transfer separately

Irrigation, drinking water, industrial processes

Eastern states: attached to land; Western states: separate permits

Price per acre-foot; agricultural productivity impact

Surface/Subsurface Rights

Everything at ground level vs. everything below foundation depth

Yes, can be severed

Surface: buildings, farming; Subsurface: foundations, utilities, mineral access

Usually unified unless minerals were historically severed

Surface: standard appraisal; Subsurface: depends on mineral content

Mineral Rights and Surface Rights

Mineral rights do not convey automatically—especially in Texas, Oklahoma, Pennsylvania, West Virginia, North Dakota, and other states with oil and gas history. Previous owners might have sold mineral rights in 1952. That sale still applies today.

Who owns mineral rights on property? You won't know without title research. Standard title insurance policies exclude mineral rights unless you specifically pay for a mineral rights endorsement (which itself requires a separate examination of mineral conveyances going back 50+ years).

Deeds often include language like "surface estate only" or "excepting and reserving all oil, gas, and other minerals." If you see that, someone else owns what's underground.

Leasing mineral rights differs fundamentally from selling them. Here's how mineral leases typically work:

Energy company pays a bonus (upfront payment per acre, often $500-$5,000/acre depending on geology)

Lease runs for a primary term (usually 3-5 years)

If the company drills a producing well, the lease continues as long as production continues

Landowner receives royalties (percentage of production revenue, typically 12.5%-25%)

When the lease expires without production, rights revert to the landowner who can negotiate a new lease

Surface owners must accommodate reasonable mineral extraction even when they don't own the minerals. An energy company can drill wells, build access roads, and install pipelines. They owe compensation for surface damages, but they have the legal right to access their minerals.

This creates conflicts. Your dream home site might have beautiful views and perfect privacy. Then an energy company shows up with rights to the minerals below, drills six wells on your property, and runs trucks past your house for three months. Legally, you can't stop them if they own the minerals.

Water Rights in Real Estate

Water rights in real estate operate under completely different systems depending on geography. Eastern states generally follow riparian doctrine. Western states use prior appropriation. They're almost opposite approaches.

Riparian rights (eastern U.S.): If your property borders a stream, river, or lake, you have the right to reasonable use of that water. These rights transfer automatically with the land—you can't sell water rights separately from riparian property. Reasonable use means you can't deplete the water source or significantly harm downstream users.

Prior appropriation (western U.S.): Water rights exist independently from land ownership. The system works on seniority—"first in time, first in right." A rancher who filed for water rights in 1882 has senior rights over everyone who came later. During droughts, senior rights holders get their full allocation before junior rights holders get anything.

In prior appropriation states, you can own land without any water rights. You can also own water rights to a river 50 miles away without owning any land near that river. Water rights are separate property that can be bought, sold, and leased independently.

Transferring these rights requires state engineer approval. States scrutinize transfers to prevent: - Injury to other water rights holders - Changes in historical use that affect return flows - Moving water out of the watershed to the detriment of the basin

Water rights in Colorado's Front Range can sell for $40,000-$100,000 per acre-foot. High-quality senior rights go even higher. In parts of the West, water rights are more valuable than the land itself.

Subsurface rights vs surface rights becomes relevant with groundwater. Some states treat groundwater as part of the surface estate—pump whatever you want from wells on your land. Others regulate it like surface water, requiring permits and limiting pumping. Texas follows the "rule of capture" (pump freely). Arizona requires permits and limits pumping in designated Active Management Areas.

Common Air Rights Scenarios and Examples

Let's look at real transactions that show how this works:

Grand Central Terminal, New York City: Back in 1968, Penn Central Railroad owned Grand Central and wanted to build a 55-story office tower on top of it. The city's landmarks commission rejected the plan to preserve the Beaux-Arts terminal. Penn Central sued, claiming the city had "taken" their air rights without compensation.

The Supreme Court said no—the city could restrict development on landmarks. But New York had to provide a mechanism for Penn Central to recapture value. The solution? Let them transfer over 1 million square feet of development rights to nearby parcels. Penn Central sold those rights in chunks over the following decades, eventually generating over $250 million. Grand Central still stands. Neighboring buildings got taller.

St. Patrick's Cathedral air rights: The Archdiocese of New York owns the Gothic Revival cathedral sitting on Fifth Avenue in Midtown. Historic building, never going to be demolished. But it sits on a 54,000-square-foot lot in one of the world's most expensive real estate markets.

Between 2013 and 2021, the Archdiocese sold approximately 300,000 square feet of air rights in multiple transactions to developers of luxury residential towers on adjacent parcels. Total value? Roughly $200 million. The cathedral got funding for a major restoration (including $177 million just for exterior repairs) without borrowing or selling any property. Developers got the extra height they needed for ultra-luxury condos selling at $5,000-$7,000 per square foot.

Hudson Yards, Manhattan: This 28-acre development on Manhattan's West Side is built over active rail yards. The Metropolitan Transportation Authority owns the rail yards and needed them operational—you can't shut down critical infrastructure for a real estate project.

Solution: Developers purchased over 3 million square feet of air rights from the MTA for approximately $1 billion. They built platform structures over the rail yards, with trains running underneath. The MTA got $1 billion for transit improvements. Developers got one of the largest private real estate developments in U.S. history (18 million square feet of mixed-use space).

Chicago's Millennium Park: The park sits on top of an active rail yard and parking garage. The City of Chicago purchased air rights from the railroads to build the park structure above while commuter trains continue operating 40 feet below the surface. Park visitors walk on the roof of a transportation hub—most never realize trains are running beneath them.

Small-scale deal in Seattle: A restaurant owner wanted to expand vertically but had maxed out their FAR. The neighboring property—a single-story nonprofit office—had unused development rights. The restaurant owner purchased 4,000 square feet of air rights for $180,000 ($45/sf). This allowed them to add a third floor, doubling their dining capacity. The nonprofit used the $180,000 for building improvements and program expansion. No lawyers needed to fight, no zoning variances required—just two neighbors making a deal that benefited both.

Author: Daniel Crosswell;

Source: redmonpestmgt.com

Air Rights Valuation and Market Considerations

Pricing air rights involves educated guesswork backed by analysis. Values swing wildly based on:

Zoning specifics: Rights in residential high-rise zones sell at premiums compared to commercial-only zones. If the city offers bonus FAR for including affordable housing or public plazas, those bonus rights increase value by 20-40% because they're essentially free square footage.

Physical constraints: Air rights only help if the receiving site can actually use them. A 3,000-square-foot lot hemmed in by tall buildings on all sides might struggle to build additional floors even with purchased air rights—there's simply no room. Developers analyze structural feasibility, foundation capacity, and elevator core requirements before committing.

Market cycles: In boom times, Manhattan air rights have traded at $400+ per square foot. In downturns, prices fall to $150-200. Chicago sees similar patterns but at lower absolute prices ($80-150/sf during booms, $30-60/sf during busts). Timing matters enormously.

Transfer restrictions: Air rights limited to adjacent parcels sell at 30-50% discounts compared to freely transferable rights. Why? Limited buyer pool. You can only sell to immediate neighbors, giving them negotiating leverage.

Development timeline: Developers buying air rights for active projects pay more than speculators betting on future development. Active buyers need the rights now and pay accordingly. Speculators want discounts reflecting holding period risk.

Appraisal methods tackle this from different angles:

Sales comparison: Gather recent air rights transactions within the same zoning district. Adjust for timing, exact location, and FAR transferability. This works well in active markets like Manhattan or Downtown Miami where transactions happen regularly. In smaller cities with thin markets, finding comparable sales proves difficult.

Residual method: Start with the developer's project pro forma. What's the finished building worth? Subtract hard costs, soft costs, financing costs, profit margin, and land value. Whatever's left is the maximum the developer can pay for air rights while meeting their return threshold. This gives a ceiling price from the buyer's perspective.

Income approach: Calculate the additional revenue from extra floors (rental income or condo sales). Subtract the incremental costs to build those floors. Discount the net income to present value using an appropriate cap rate. This method works best for income-producing properties.

Tax treatment varies. The IRS generally treats air rights sales as capital gains for sellers (assuming they've held the property long-term). Buyers capitalize the purchase price as part of their development cost basis, depreciating it over 39 years for commercial property or 27.5 years for residential.

Some municipalities assess property taxes on unused air rights, though this is controversial. New York experimented with this concept. The theory: unused development capacity has value, so it should be taxed like other property. The reality: it's complicated to assess and creates political backlash from property owners who feel they're being taxed on something they might never use.

Current market trends show strong demand in gateway cities where land scarcity makes air rights essential. Secondary markets like Denver, Austin, and Nashville are implementing or expanding TDR programs as they manage growth. Interestingly, climate-related zoning changes—particularly coastal retreat policies that restrict development in flood zones—may create new air rights markets as development capacity concentrates in safer inland areas.

Author: Daniel Crosswell;

Source: redmonpestmgt.com

Frequently Asked Questions About Air Rights

Can air rights be sold separately from the land?

Yes, in cities with TDR programs or to adjacent property owners. The sale involves recording a permanent easement that restricts future development on your property while conveying building capacity to the buyer. Not every jurisdiction allows this, though. Some municipalities prohibit severing air rights from the underlying land, requiring them to stay bundled together. Before attempting to sell air rights, check local zoning ordinances and talk to a real estate attorney familiar with your city's regulations. Even where transfers are allowed, you'll likely need municipal approval and compliance with specific TDR program requirements.

Do mineral rights convey when selling property?

Only if the deed specifically includes them and they haven't been previously severed. In states with oil, gas, or mineral production history, separated mineral rights are common. Standard warranty deed language like "together with all appurtenances" typically includes minerals unless there's explicit exception language. The problem? Someone might have severed the minerals in 1963. That conveyance still controls today, even if it happened before your seller owned the property. Always request a mineral rights certification or title opinion before closing, especially in Texas, Oklahoma, North Dakota, Pennsylvania, and West Virginia. Standard title insurance policies exclude mineral rights coverage unless you pay extra for a specific endorsement.

How are air rights different from subsurface rights?

Air rights control vertical space above ground level—what you can build upward. Subsurface rights control everything below the surface—minerals, foundations, underground storage, utility lines. Both can be severed and sold separately from surface rights, but they're governed by different legal systems. Air rights fall under land use and zoning law. Subsurface rights (particularly mineral rights) follow mineral law and property statutes developed for resource extraction. Measurement differs too: air rights use FAR or height limits, while subsurface rights might extend to specific depths or geological formations. Practically speaking, air rights matter in dense cities where building tall creates value. Subsurface rights matter in energy states where oil, gas, or minerals exist.

Who typically buys air rights?

Real estate developers with active projects represent 80% of buyers. They need additional building capacity to make their projects economically viable. Institutional investors occasionally buy speculatively, betting that neighborhood appreciation or zoning changes will increase values—though this is riskier given the specialized nature of the asset. Adjacent property owners sometimes buy defensively to prevent neighbors from selling to developers who might build tall structures that block their views or sunlight. In rare cases, corporations purchase air rights for future headquarters expansion, and billboard companies acquire rights for advertising structures. The buyer profile depends heavily on location—Manhattan air rights attract international capital and sophisticated developers, while small-city transactions typically involve local players.

Can you lease air rights like mineral rights?

Yes, though it's less common than outright sales. Ground lease structures sometimes separate land ownership from building ownership, with the building owner effectively leasing air rights from the landowner for 99 years. Billboard companies routinely lease air rights for 10-30 year terms with renewal options, paying monthly rent for the right to place advertising structures above buildings. Some institutional landowners prefer leasing to maintain long-term control while generating current income. Developers generally prefer buying air rights outright to avoid ongoing lease payments and secure permanent rights. If you're considering an air rights lease, negotiate carefully around what happens if zoning changes, whether you can sublease or transfer the lease, termination conditions, and renewal terms.

What happens to air rights when zoning changes?

Zoning changes can create or destroy air rights overnight. Upzoning—when the city increases permitted density or height—creates additional air rights that didn't exist before. Property owners get a windfall because they can suddenly build more or sell more. Downzoning—reducing permitted density—can eliminate existing air rights. Most jurisdictions grandfather legal nonconforming rights, meaning if you could have built 20 stories yesterday but new zoning only allows 15, you typically keep the right to build 20. Some cities don't grandfather, though, or they limit how long you can preserve those rights without acting. If you've already sold air rights and the receiving site gets downzoned before construction, the transaction usually remains valid under vested rights doctrine, though expect potential litigation. Smart property owners monitor comprehensive plan updates and attend public hearings on rezoning proposals that might affect their air rights value.

Property ownership isn't flat—it's three-dimensional. Air rights turn that vertical dimension into real economic value, particularly in cities where land scarcity pushes development upward.

For property owners, this means the space above your building might be worth more than you think. A modest church or theater sitting on a downtown lot could have millions in unused development rights. Religious institutions across the country have discovered this and used air rights sales to fund restorations, expand programs, or build financial reserves—all without selling or demolishing their buildings.

For buyers, it means scrutinizing what rights actually transfer with your purchase. Are the air rights included? Did a previous owner sell them in 1985? Is there a recorded restriction limiting future development? These questions matter because discovering after closing that someone else owns your air rights can torpedo your plans and destroy value.

For developers, air rights represent essential tools in land-constrained markets. You can't assemble enough contiguous land for a major project in Midtown Manhattan or Downtown San Francisco at any reasonable price. But you can buy a smaller footprint and purchase air rights from surrounding properties to build the density you need.

The key distinction between air rights, mineral rights, water rights, and surface rights is that each component operates under different legal frameworks, markets, and valuation methods. Air rights flow from zoning codes and land use planning. Mineral rights stem from resource extraction law and commodity markets. Water rights follow regional systems (riparian vs. prior appropriation) shaped by hydrology and agriculture. Understanding which rights you need, confirming they're included in your transaction, and knowing how they interact with neighboring properties separates successful real estate deals from expensive mistakes.

As urban density increases and land becomes scarcer, air rights markets will expand beyond traditional gateway cities. Mid-sized metros are implementing TDR programs to manage growth while preserving historic structures and open space. Climate adaptation—particularly in coastal areas—may push development inland, creating new air rights markets in previously overlooked neighborhoods.

The principles here give you a foundation. Local execution requires experienced professionals—zoning attorneys who know your city's codes, title companies that can research historical conveyances, and appraisers who understand how to value these unusual assets. Air rights transactions involve complexity, but they've moved from exotic novelties to mainstream tools in modern real estate development.

Fee simple absolute represents the highest form of property ownership in American law, granting owners the broadest possible rights. Unlike conditional ownership or leases, this estate gives maximum control over use, transfer, and inheritance of real property with no automatic termination conditions

When someone dies, their estate is either testate or intestate. Dying testate means leaving a valid will that directs asset distribution. Dying intestate means state law decides everything. Understanding this distinction determines who controls your legacy

Right of survivorship automatically transfers a deceased owner's property interest to surviving co-owners, bypassing probate. This guide explains how it works, compares joint tenancy vs tenancy in common, covers tax implications, and shows how survivorship rights override wills

Real estate law governs property ownership, transfer, and use in the United States. This comprehensive guide explains foundational legal principles, transaction structures, common issues, and when to seek legal help for residential and commercial real estate matters

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to real estate law, property rights, leases, liens, zoning, landlord-tenant disputes, and litigation.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal outcomes may vary depending on jurisdiction, property type, and individual circumstances.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified attorneys or real estate professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.