Two people shaking hands in front of a suburban house with a For Sale sign, documents on a table between them, symbolizing a land contract real estate deal

So you're buying or selling a home through a land contract, and now you're wondering: who actually cuts the check to the county when property tax bills arrive?

Here's what catches most people off guard. Even though your contract probably says the buyer pays taxes, the county still considers the seller the legal owner. That means if taxes don't get paid, the county comes after the seller first—regardless of what your private agreement says.

I've seen buyers assume they're off the hook because they're "just making payments." I've also watched sellers discover $12,000 in back taxes and penalties because they trusted a buyer to handle payments without ever checking. Both situations end badly.

The real issue? You've got split ownership. The buyer lives there and acts like an owner. The seller's name stays on the deed. And the property tax assessor doesn't care about your arrangement—they just want their money. Let's break down who actually pays what, and more importantly, what happens when someone drops the ball.

What Is a Land Contract and How Does It Work

Think of a land contract as an IOU for real estate. The seller acts as the bank.

Instead of getting a mortgage from Wells Fargo or Chase, you're making payments directly to the person who owns the house. They keep the deed in their name. You move in and start making payments. After you've paid everything off—could be five years, could be twenty—they hand over the deed and you become the official owner.

The mechanics work like this: You and the seller negotiate a price (let's say $180,000). You put down $15,000. You agree to pay $1,450 monthly at 7% interest for fifteen years. You sign the land contract. You get the keys. The seller keeps the deed locked in their safe deposit box.

Every month, you send that payment. Part goes toward the $165,000 you still owe. Part covers the interest. And that deed? It doesn't change hands until payment number 180 clears.

This setup appeals to buyers who've been turned down by banks. Maybe your credit score is 580. Maybe you're self-employed and can't document income the way lenders want. Maybe you just got divorced and your debt-to-income ratio is temporarily wrecked. Traditional lenders say no. But a motivated seller might say yes.

Sellers like land contracts because they earn interest instead of taking a lump sum. In a slow market, offering seller financing can attract buyers when nothing else moves the property. Plus, if you default, they can take the house back faster than a bank could foreclose on a mortgage.

But here's the problem: neither party is a financial institution. There's usually no escrow department, no automated payment processing, no team monitoring whether property taxes get paid. That's where things get messy.

Author: Olivia Carringt;

Source: redmonpestmgt.com

Property Tax Responsibility in Land Contracts

Ask ten real estate attorneys who pays property taxes on a land contract, and you'll get ten variations of "it depends." State laws differ. Individual contracts vary wildly. And what the contract says doesn't always match what the county enforces.

What the Contract Says vs. What the Law Says

Pull out your land contract and find the section about property taxes. Most agreements include language like "Buyer shall pay all property taxes when due" or "Buyer assumes responsibility for all tax obligations." Seems clear enough, right?

Except the county treasurer's office doesn't read your contract. When they look up the property address in their system, they see the seller's name as the owner of record. That's who gets the tax bill. That's who they'll sue if taxes go unpaid. Your private agreement with the buyer is legally meaningless to them.

I know a seller in Ohio who learned this the hard way. His contract clearly stated the buyer would pay all taxes. The buyer lived in the house for three years and never paid a dime in property taxes. The county filed a lien, started foreclosure proceedings, and came after the seller. The seller had to pay $11,400 in back taxes plus penalties to save the property. Sure, he could sue the buyer for breach of contract, but the buyer had already disappeared. The seller was out the money either way.

Some contracts try to protect sellers by requiring buyers to submit proof of payment within fifteen or thirty days of each tax deadline. Smarter contracts let the seller pay delinquent taxes and add that amount to the balance owed, plus interest. But even these provisions don't change the fundamental problem: the county considers the seller responsible, period.

When Buyers Pay Property Taxes

In probably 90% of land contracts I've reviewed, the buyer takes on property tax payments. Makes sense—they're living there, using the schools, calling the fire department if needed. They're benefiting from whatever those tax dollars fund.

You'll see three common payment arrangements. The first and most popular: the buyer pays the county directly. When that tax bill shows up in December (or whenever your county sends them), the buyer writes a check to the treasurer's office. Then—and this matters—they're supposed to send proof to the seller. A copy of the cancelled check. A receipt from the county. Something showing they actually paid.

Reality check: buyers forget to send proof. They assume if they paid, everything's fine. Meanwhile, the seller has no idea whether taxes got paid until they either ask or the county sends a delinquency notice.

The second method builds property taxes into the monthly payment. Say your annual taxes are $3,600. You pay the seller an extra $300 per month. The seller collects this money all year, then pays the county when the bill arrives. This works like traditional mortgage escrow but depends entirely on the seller actually setting that money aside instead of spending it.

The third approach is rarer: the seller pays the county directly, then bills the buyer separately for reimbursement. Creates extra paperwork. Often leads to disputes about timing. "I'll reimburse you next month when I have the money" turns into arguments.

When Sellers Remain Responsible

Some land contracts keep property tax responsibility with the seller. This happens more often on shorter-term deals or raw land sales.

A seller might keep this obligation to ensure taxes get paid. They build the tax cost into the monthly payment amount without breaking it out separately. The buyer pays $1,800 monthly, never knowing that $250 of that covers property taxes. The seller handles payment to the county. Simpler for the buyer, more control for the seller.

But here's the thing: sellers never escape tax liability, even when the contract assigns it to the buyer. Until that deed transfers, the county views the seller as responsible. If the buyer stops paying, the seller must cover taxes during whatever legal process is required to reclaim the property—could be forfeiture, could be foreclosure, depending on your state. Let those taxes slide while you're dealing with a defaulted buyer, and you could lose the whole property to a tax sale.

Author: Olivia Carringt;

Source: redmonpestmgt.com

Land Contract vs Mortgage: Key Differences in Tax Obligations

The property tax situation looks completely different when you compare land contracts to conventional mortgages. The difference comes down to timing and legal ownership.

Get a mortgage from a bank? You become the legal owner immediately. You sit down at closing, sign roughly four thousand documents, and walk out with a deed in your name. The bank doesn't own your house—they just have a lien on it. The county property records show you as owner from day one. Tax bills arrive with your name on them. You pay them. There's zero confusion about responsibility.

Banks protect themselves through escrow accounts. Your monthly mortgage payment includes principal, interest, property taxes, and insurance (PITI). The bank collects one-twelfth of your annual property tax bill every month. When December rolls around and taxes come due, the bank pays the county from your escrow account. You never have to remember deadlines or worry about missing payments.

If somehow you refuse to escrow and then don't pay property taxes, the bank finds out fast. They pay the taxes themselves to protect their collateral, then add that amount to your loan balance. Banks don't let tax foreclosures happen—they have way too much money at stake.

Land contracts operate without these safeguards. The seller usually isn't equipped to manage escrow accounts. They're just regular people who sold a house with owner financing. They don't have automatic payment systems or staff monitoring county tax records. If the buyer forgets or refuses to pay property taxes, months can pass before anyone notices.

The tax deduction situation also differs. Mortgage holders clearly qualify to deduct property taxes on Schedule A because they're the legal owners. Land contract buyers occupy this weird gray area—they can usually deduct taxes as equitable owners, but they need better documentation and might face IRS questions.

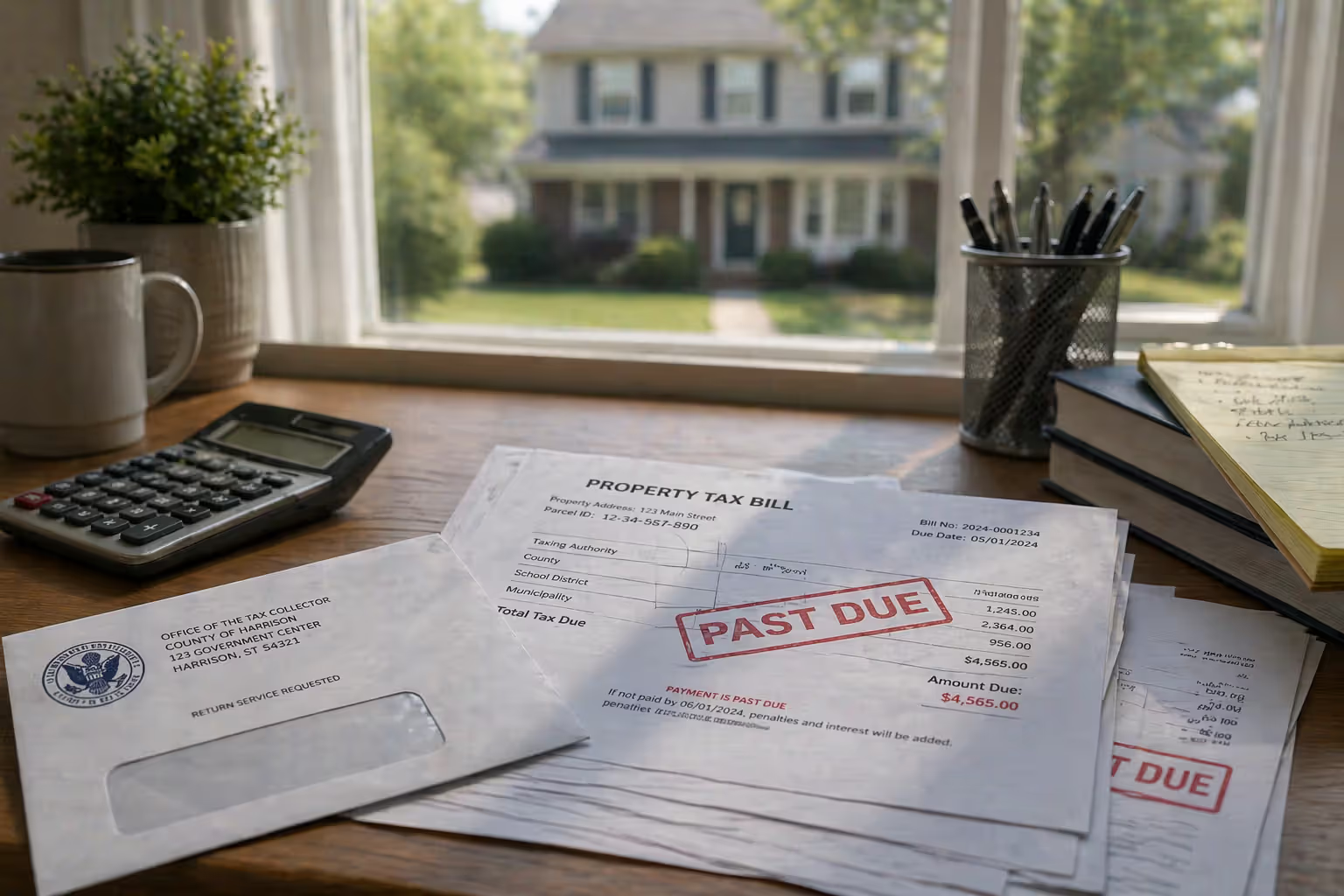

What Happens If Property Taxes Aren't Paid

Unpaid property taxes trigger a nightmare scenario for everyone involved in a land contract. Counties have extraordinary collection powers, and property tax liens trump almost everything else—including whatever rights you have under your land contract.

Let's say property taxes don't get paid. First come the penalties. Most counties tack on 1.5% monthly interest. Some add flat penalty fees on top. A $4,000 tax bill becomes $4,800 after just a few months. Let it ride for a year? You're looking at $4,600 to $4,800 depending on your county's penalty structure.

But it gets worse. After taxes remain unpaid for a certain period—anywhere from one to three years depending on state law—the county starts tax foreclosure proceedings. They can literally sell your property at a public auction to recover the unpaid taxes. Doesn't matter how much equity you have. Doesn't matter if you've paid $80,000 toward a $150,000 purchase price.

Tax foreclosure destroys both parties' interests simultaneously. The buyer loses all the money they've paid toward the purchase. The seller loses the property without receiving the remaining balance owed. If the property sells at tax sale for $50,000 to cover $8,000 in taxes, everyone walks away with nothing.

I watched this happen to a couple in Michigan. They'd paid $45,000 over four years on a $120,000 land contract. They thought the seller was handling property taxes from their monthly payments. The seller thought the buyers were paying directly. Neither actually paid. The county sold the property at tax auction for $62,000 to cover $9,500 in back taxes and penalties. The buyers lost their $45,000. The seller lost a property worth $120,000 and received nothing. All over a miscommunication about who was paying taxes.

For buyers, failing to pay property taxes often triggers the default clause in your contract even if your monthly payments are current. Most land contracts define default broadly: "failure to pay property taxes, maintain insurance, or keep the property in good repair constitutes default allowing seller to terminate this agreement." Miss one tax payment deadline and technically the seller can start forfeiture proceedings.

Sellers face exposure from two directions. The county pursues them personally for payment since they're the legal owner. Collection agencies call. Liens attach. Meanwhile, the property becomes unsellable. Even if the buyer completes all payments, you can't deliver clear title with a tax lien attached. You'll have to satisfy that lien before conveying the deed.

Smart sellers write specific protections into their contracts: "Seller may pay any delinquent property taxes to protect the property and add such amounts to the principal balance owed, bearing interest at 2% above the contract rate." This lets you cure the problem and recover your costs.

Author: Olivia Carringt;

Source: redmonpestmgt.com

Buyer and Seller Rights Regarding Property Taxes

Both parties in a land contract have specific rights related to property taxes, though most people don't realize these protections exist. Knowing what you can and can't do prevents disputes and protects your investment.

Buyers hold several important rights. You can pay property taxes directly to the county even if your contract says payments go through the seller. As the equitable owner in possession, you have standing to protect your interest by ensuring taxes get paid. Can't force the seller to accept this arrangement? Pay the county anyway, keep your receipt, and offset that amount from future contract payments.

You also have the right to verify tax status anytime. Call your county treasurer's office or check their website. Most counties now show payment history online. Just enter the property address. You can see whether taxes are current, when the last payment was made, and whether any penalties have accrued. Do this annually at minimum, even if the seller is supposedly handling taxes from your monthly payments.

If you discover unpaid taxes, you can demand proof of payment from the seller. If they can't provide it, pay the county yourself immediately. Document everything. Send the seller a certified letter explaining what you paid and why you're deducting that amount from future payments. This creates a paper trail if disputes arise later.

Sellers have rights too. You can declare the buyer in default for failure to pay property taxes as required. Your land contract should specify this clearly. Once you've declared default, you can start forfeiture proceedings (in most states) or foreclosure (in states that treat land contracts like mortgages for enforcement purposes).

You can also cure tax delinquencies and bill the buyer. Let's say you discover the buyer hasn't paid $6,000 in property taxes. You can pay that amount to prevent tax foreclosure, then add $6,000 to the principal balance owed under the contract. Most sellers include language allowing them to charge interest on these amounts—often 2% to 5% above the contract interest rate.

Requiring annual proof works better than fixing problems after they occur. Include a provision requiring the buyer to submit proof of tax payment within thirty days of the due date. If they don't, you can pay the taxes yourself and add the cost to their balance. This keeps you informed and creates consequences for non-compliance.

Third-party escrow arrangements offer the best protection for everyone. A title company or escrow agent collects the monthly payment, sets aside the tax portion, and pays the county when taxes come due. Costs around $300 to $500 annually depending on your location, but eliminates all disputes and ensures compliance. Both parties sleep better knowing a professional is handling it.

Land Contract vs Rent to Own: Tax Payment Differences

Author: Olivia Carringt;

Source: redmonpestmgt.com

Land contracts get confused with rent-to-own deals constantly, but the property tax handling differs significantly. Understanding this distinction matters if you're comparing financing options.

In a rent-to-own arrangement—whether structured as a lease-option or lease-purchase—you're a tenant first, buyer later. You sign a lease and pay rent monthly. Part of that rent might be credited toward a future purchase, but you're renting right now. The seller maintains complete ownership, both legal and equitable. You have an option (or obligation, depending on the agreement) to buy later.

Because the seller remains the full owner during the rental period, they pay property taxes. Has to be this way legally. They're the landlord. It's their property. The county sends tax bills to them. This follows standard landlord-tenant rules—owners pay property taxes, tenants pay rent.

Your rent might be higher than market rate specifically because the seller is paying property taxes, insurance, and maintenance while giving you credits toward purchase. But you don't write checks to the county treasurer. You don't get tax bills in your name. You're not responsible if the landlord fails to pay—though a tax foreclosure would obviously terminate your lease and option rights.

Land contracts transfer equitable ownership immediately. You're not renting. You're buying on an installment plan. The difference matters for property tax responsibility. Since you're an owner (equitable if not legal), you typically assume all owner responsibilities including property taxes.

From a practical standpoint, rent-to-own tenants have zero control over property tax payments. Land contract buyers usually have direct responsibility and control. You can pay the county yourself. You monitor whether taxes are current. You face consequences if taxes go unpaid.

The tax deduction angle differs dramatically. Rent-to-own tenants can't deduct property taxes on their tax return because they don't own the property, period. Land contract buyers often qualify for property tax deductions as equitable owners. That difference can mean $1,000 to $3,000 annually in tax savings depending on your tax bracket and property tax amount.

Risk profiles differ too. If a rent-to-own landlord doesn't pay property taxes, you might lose your option rights when the property sells at tax auction, but you're not personally liable for the debt. Land contract buyers face direct consequences—you could lose your entire investment and all accumulated equity if taxes go unpaid and the county forecloses.

IRS and Tax Implications of Land Contracts

Most land contract disasters I see stem from the same problem: nobody actually reads the tax payment clause until something goes wrong.I had a case last year where the buyer assumed monthly payments covered everything. The seller assumed the buyer was paying taxes separately. The contract said 'buyer responsible for taxes' but didn't specify how or when. Three years later, the county filed a $16,000 lien for unpaid taxes and penalties. Both parties called me furious at each other, but really they were both at fault for not clarifying the arrangement upfront.Require the buyer to submit proof of tax payment within twenty days of each deadline. Give the seller the right to access county records online to verify payment.

— Michael Chen

Most importantly, include language allowing the seller to pay delinquent taxes and add those amounts to the principal balance at an increased interest rate—maybe 3% above your contract rate. This protects the seller's collateral while creating a real financial consequence for the buyer's non-payment.Trust but verify. Even if you're paying the seller monthly and they promise to handle property taxes, check the county records annually. Takes five minutes online. I've seen too many buyers discover unpaid taxes only when they're three years behind and facing foreclosure. By then, the damage is done and the seller might not have the money to cure the delinquency even if they wanted to

The IRS has specific rules about how land contracts get treated for tax purposes, affecting both parties' returns and creating deduction opportunities most people miss.

For sellers, the IRS treats land contracts as installment sales. Instead of recognizing your entire gain in the year you sell, you report profit gradually as you receive payments. Sell a property for $200,000 that you bought for $120,000? That's $80,000 in gain. On an installment sale, you report the gain proportionally as payments come in. Receive 10% of the principal this year? You report 10% of the gain.

This treatment can drop you into a lower tax bracket. Taking $80,000 in gain all at once might push you into the 24% federal bracket. Spreading it over ten years might keep you at 12%. The tax savings can be substantial.

But sellers must report the interest they receive as income every year. That $7,000 you collected in interest payments? That's ordinary income, taxed at your regular rate. You can't defer it like the capital gain.

Property tax deductibility for sellers depends on who actually pays. If your contract requires you to pay property taxes from the buyer's monthly payments, you can deduct those taxes as an expense. If the buyer pays the county directly, you can't deduct them because you didn't pay them. This creates a tax incentive for sellers to retain tax payment responsibility—you can deduct the taxes while earning interest income from the buyer.

Buyers occupying the property as their primary residence can deduct property taxes paid on Schedule A if they itemize. The IRS recognizes land contract buyers as equitable owners for this purpose. The catch? Documentation requirements are stricter.

You need proof you actually paid the taxes. Keep cancelled checks showing payment to the county treasurer. Save receipts from the county showing the payment date and amount. If your monthly payment to the seller includes a tax component but the seller pays the county, you cannot deduct those taxes—the seller can because they're the one who paid.

The mortgage interest deduction also applies to land contract buyers, but requires specific documentation. You need Form 1098 from the seller, or you must attach a statement to your return showing the seller's name, address, Social Security number (or employer ID number), and the total interest paid. Many sellers don't issue Form 1098 because they're not familiar with the requirement. You can still claim the deduction, but you need to follow IRS documentation rules precisely.

Property tax increases during the contract typically fall on buyers unless your agreement specifically caps your obligation. Standard contract language says "Buyer shall pay all property taxes and assessments" or similar wording. "All" means all—including increases from county reassessments, millage rate hikes, or new special assessments for sewer improvements or road work.

Budget accordingly. A property with $3,000 annual taxes when you sign might have $4,200 in taxes five years later. Happened to buyers in neighborhoods experiencing rapid appreciation—their property values jumped 40%, triggering reassessments that spiked their tax bills. The land contract didn't cap their obligation, so they had to pay the increase.

Sellers who previously rented the property need to watch for depreciation recapture issues. If you've been depreciating the property as a rental and now sell via land contract, you'll owe depreciation recapture taxes when you report the installment sale income. This can create a surprise tax bill that reduces the benefits of installment sale treatment. Definitely consult a CPA before structuring the deal.

Tax Responsibility by Financing Type: A Comparison

Financing Method

Who Writes the Check to the County

Who Can Deduct Taxes

Who Legally Owns the Property

What Happens if Nobody Pays

Land Contract

Usually the buyer, though the seller stays legally liable to the county

Buyer (as equitable owner with proper documentation)

Seller keeps the deed; buyer has equitable interest and possession rights

County forecloses and both parties lose everything—buyer's payments and seller's equity

Traditional Mortgage

Buyer (the legal owner from day one)

Buyer

Buyer owns the property; bank holds a lien as security

Bank typically pays the taxes to protect their collateral, then adds the amount to your loan balance

Rent-to-Own

Seller/landlord (still the full owner during rental period)

Seller/landlord

Seller retains complete ownership; tenant just has option rights to buy later

Tenant's option rights terminate but they face no personal tax liability

Frequently Asked Questions

Can a buyer deduct property taxes on a land contract?

Yes, buyers can deduct property taxes they actually pay, but documentation matters more than with traditional homeownership. You're claiming the deduction as an equitable owner, which raises IRS scrutiny. Keep cancelled checks or money order receipts showing payment directly to the county treasurer. Save copies of the tax bills and county receipts. If you pay the seller monthly and they pay the county, you can't deduct it—the seller can, because they're the one who actually paid. Some buyers mistakenly claim deductions for tax amounts included in monthly payments, then get audited when they can't prove they paid the county directly. Consult a tax preparer familiar with land contracts to ensure you're documenting correctly.

Who holds the deed when property taxes are owed on a land contract?

The seller keeps the deed during the entire contract period regardless of property tax status. This doesn't change even if taxes become delinquent. The county lists the seller as the legal owner and pursues them for unpaid taxes, yet the seller can't transfer the deed until the buyer completes all payments. This creates the central tension in land contract tax liability—the person legally responsible (seller) doesn't control whether taxes get paid, while the person with the obligation (usually the buyer) isn't the owner in the county's eyes. The deed only transfers after you've made every payment specified in the contract and satisfied all other obligations including property taxes. Until then, it stays in the seller's possession.

What happens if the seller doesn't pay property taxes on a land contract when they're supposed to?

Buyers have several options when sellers fail to pay taxes they contractually agreed to pay. Pay the county directly yourself first—this protects your equitable interest from tax foreclosure. Get a receipt. Then notify the seller in writing (certified mail, return receipt) that you paid their obligation and you're deducting that amount from future monthly payments. Your land contract might already authorize this offset. If not, you're still entitled to reimbursement. You can sue for breach of contract if the seller refuses to reimburse you or accept the offset. In extreme cases where the seller's non-payment threatens your ability to obtain the property, you might have grounds to rescind the entire contract and recover your payments. Document everything meticulously.

Are property taxes escrowed in a land contract?

True escrow arrangements are uncommon in land contracts, but they're the safest option. Traditional mortgages involve banks with escrow departments and automated systems. Land contracts usually involve individuals who lack this infrastructure. However, you can set up third-party escrow through a title company or attorney's trust account. The escrow agent collects your monthly payment including a tax reserve, holds those funds separately, and pays the county when taxes come due. Costs $25 to $40 monthly plus setup fees, but it eliminates disputes and ensures compliance. Without formal escrow, some contracts approximate this by having the buyer pay the seller monthly with the understanding the seller will pay taxes, but nothing legally segregates those funds or guarantees payment.

Can a land contract be foreclosed for unpaid property taxes?

Absolutely, and property tax foreclosure takes priority over your land contract rights. Counties have superior authority to collect property taxes through foreclosure and sale. If taxes remain unpaid beyond your state's redemption period (ranges from one year to three years), the county can auction the property to recover the tax debt. This tax foreclosure extinguishes both the buyer's equitable ownership and the seller's legal title. Doesn't matter if the buyer has paid $90,000 toward a $150,000 purchase—that equity disappears if the property sells at tax auction. The county gets their taxes and penalties. The high bidder gets the property. The buyer and seller get nothing. This worst-case scenario is why property tax payment is actually more critical than staying current on monthly contract payments.

Is the buyer or seller responsible for property tax increases during the contract?

Nearly every land contract I've seen puts tax increases on the buyer. The standard language requires the buyer to pay "all property taxes, assessments, and charges levied against the property," which includes increases from any source. County reassessments, millage rate increases, special assessments for infrastructure improvements—all of it typically falls on the buyer. Attempts to cap the buyer's tax obligation at the initial year's amount are rare and generally unsuccessful. Sellers won't agree because property taxes historically trend upward. Budget for annual increases of 2% to 5% in stable markets, more in appreciating areas. I know buyers in rapidly gentrifying neighborhoods whose tax bills doubled during ten-year contracts. The contract didn't cap their obligation, so they had to pay or risk default. Always assume taxes will increase and budget accordingly.

Property tax responsibility in land contracts requires more than checking a box that says "buyer pays taxes." You need explicit contract language, verification procedures, and regular monitoring to prevent catastrophic losses.

The fundamental problem isn't complicated: the county considers the seller responsible regardless of what your contract says. This split between contractual obligation and legal liability creates risk for everyone involved. Buyers can lose years of equity to tax foreclosure. Sellers can lose properties worth hundreds of thousands over a few thousand in unpaid taxes.

Prevention beats cure by a mile. Buyers should verify tax payment status annually even if you're paying the seller who's supposedly handling it. Takes ten minutes online. Check your county treasurer's website, enter the property address, confirm the current year's taxes are paid. If they're not, pay them immediately yourself and deal with reimbursement afterward. Protecting your investment matters more than whose fault it is.

Sellers need annual proof-of-payment requirements in their contracts. Don't just hope the buyer is handling it. Require receipt submission within twenty days of each tax deadline. Include language allowing you to pay delinquent taxes and add them to the principal balance at an increased interest rate. Monitor county records yourself periodically—you've got way too much at stake to operate on trust alone.

Both parties benefit from third-party escrow despite the added cost. Paying an escrow company $400 annually to manage tax payments eliminates disputes, ensures compliance, and lets everyone sleep at night. Compared to the potential loss from tax foreclosure, it's the cheapest insurance you can buy.

The tax deduction benefits are real for buyers who document properly. Save every receipt, keep every cancelled check, maintain a file proving you paid the county directly. Same applies to interest deductions—follow IRS documentation requirements precisely or risk losing the deduction in an audit.

Get professional help with contract drafting and tax planning. A real estate attorney's fee of $500 to $1,000 to draft or review your land contract prevents disasters that cost tens of thousands. A CPA's advice on deduction eligibility and reporting requirements for $200 to $400 can save you thousands in taxes or audit penalties.

Property taxes might seem like a minor detail compared to purchase price negotiations or interest rates, but I've seen more land contracts destroyed by property tax issues than by payment defaults. The couple who lost $45,000 because neither party paid taxes. The seller who paid $11,400 in back taxes because he trusted the buyer without verifying. These losses are completely preventable.

Take property tax responsibility seriously from day one. Clarify it in writing. Verify it annually. Budget for increases. Keep meticulous records. Get professional help structuring the arrangement. These simple steps prevent the catastrophic losses that turn land contracts from creative financing solutions into financial nightmares.

A sublease agreement creates a legal bridge between your existing lease obligations and someone else's temporary housing needs. Understanding the three-party relationship, securing landlord approval, and drafting comprehensive agreements protects your security deposit and rental history

A residential lease agreement creates legally binding obligations for both tenants and landlords. This comprehensive guide explains standard lease clauses, rights and responsibilities, security deposit rules, renewal processes, subletting options, and how to break a lease legally while avoiding costly mistakes

Persistent noise, odors, or encroachment from neighbors can cross the line into legal nuisance. Understand what qualifies as actionable nuisance under US law, the difference between private and public nuisance, and the legal steps to resolve disputes—from documentation to court remedies

Security deposits create confusion and conflict when tenants and landlords don't understand the rules. This comprehensive guide explains state laws, return timelines, allowable deductions, and how to resolve disputes—with practical examples and expert insights for both parties

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to real estate law, property rights, leases, liens, zoning, landlord-tenant disputes, and litigation.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal outcomes may vary depending on jurisdiction, property type, and individual circumstances.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified attorneys or real estate professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.