When someone lies, forges documents, or runs a scam to steal property or money during a real estate deal, that's real estate fraud. It's not just one type of crime—it's a whole category of schemes. Some criminals falsify mortgage applications. Others forge deeds to steal houses outright.

Here's what keeps me up at night: Americans lost over $450 million to property and rental scams in 2025, according to the FBI's Internet Crime Complaint Center. Wire fraud alone can wipe out someone's entire down payment—we're talking losses of $150,000 or more in a single transaction.

Who falls victim? Pretty much anyone, but first-time buyers and middle-class homeowners get targeted most often because they haven't seen these tricks before. Elderly property owners, people facing foreclosure, and buyers in competitive markets where everyone's rushing also face higher risk.

The perpetrators aren't always shadowy figures. Sure, organized crime rings run some operations. But dishonest real estate agents, corrupt loan officers, and opportunistic scammers who spot vulnerabilities also commit these crimes. Real estate deals involve so many people, so much paperwork, and such large money transfers that fraudsters find countless ways to slip through unnoticed. By the time victims realize something's wrong, the damage is already done.

Common Types of Real Estate Fraud Schemes

Mortgage Fraud and Application Misrepresentation

This happens when someone—could be the borrower, the loan officer, or even the real estate agent—deliberately lies on mortgage paperwork to get a loan approved or secure better terms.

Two basic flavors exist. "Fraud for property" means you're lying to buy a house you actually plan to live in. Maybe you inflate your income or hide some credit card debt to qualify. "Fraud for profit" is more sinister—criminals game the entire system to extract cash with no intention of paying it back.

I've seen cases where buyers claim $120,000 annual income when they really make $45,000. Others hide $80,000 in existing debt. Some use "straw buyers"—people who apply for loans on someone else's behalf because the real buyer has terrible credit or isn't eligible for other reasons.

Appraisal fraud tags along with many of these schemes. Here's how it works: A property's actually worth $300,000. The buyer and appraiser conspire to say it's worth $450,000. The bank loans based on that inflated value. The buyer pockets the $150,000 difference and disappears. The lender gets stuck with a property worth far less than the loan amount.

Even borrowers who commit what seems like "small" application fraud face serious trouble. We're talking foreclosure, criminal charges, and federal prosecution. It's not worth it.

Author: Daniel Crosswell;

Source: redmonpestmgt.com

Deed Fraud and Forged Documents

Imagine waking up one day and discovering someone else claims to own your house. That's deed fraud.

Criminals pull your personal details from public records—your name, property address, even your signature style from old documents. They create fake deeds with forged signatures transferring your property to themselves or shell companies they control. Then they walk into the county recorder's office, pay the filing fee, and record the fraudulent deed.

Here's the scary part: county clerks verify that documents look properly formatted and notarized, but they can't authenticate whether signatures are real. Once that forged deed gets recorded, it becomes part of the official property record.

What happens next? The fraudster takes out loans against your property, sells it to someone who has no idea it's stolen, or even tries to evict you from your own home. Vacant properties make easy targets. So do homes owned by elderly people or properties with paid-off mortgages—nobody's monitoring them closely, so criminals can operate longer before getting caught.

Most legitimate owners find out only when foreclosure notices arrive for loans they never took out. Or when strangers show up claiming they bought the house. It's a nightmare.

Title Fraud and Ownership Identity Theft

This scheme takes deed fraud to another level. Instead of just forging documents, criminals actually impersonate the property owner.

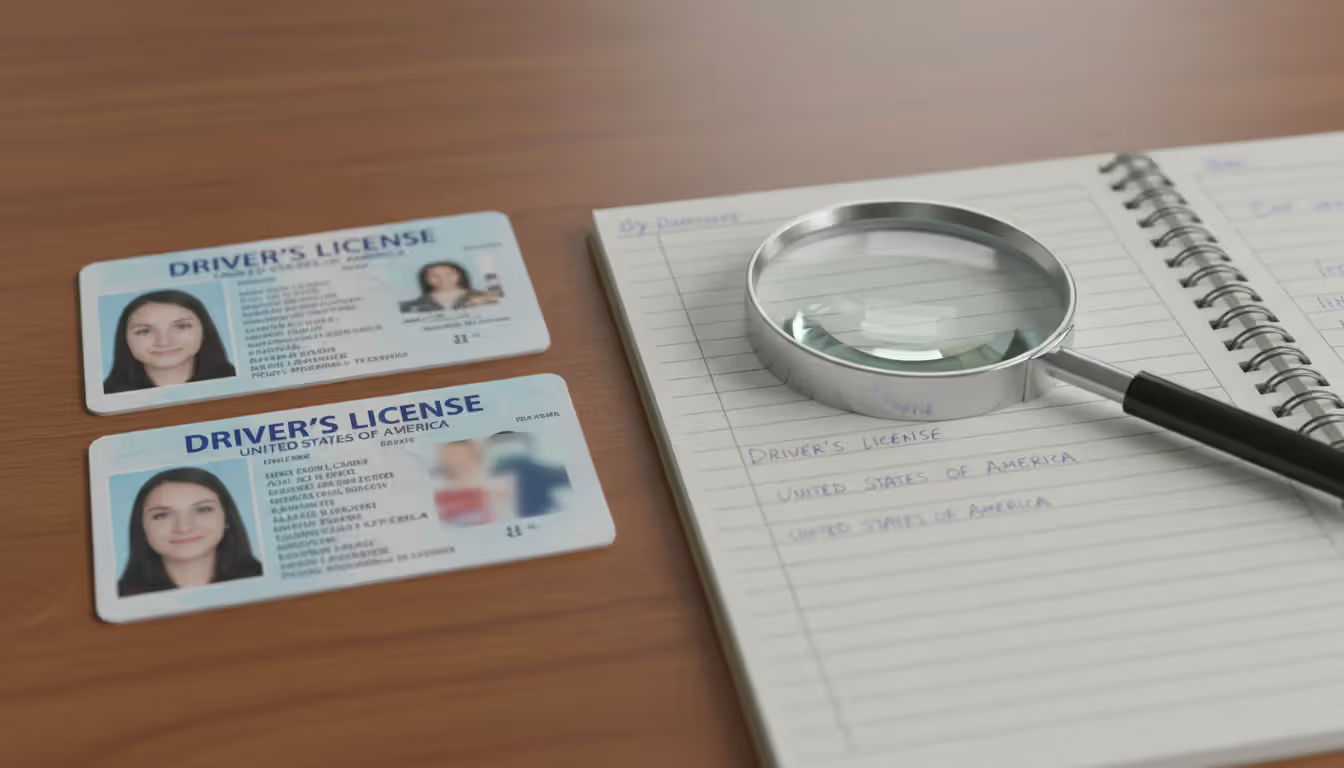

They create fake driver's licenses and identification matching your name. Then they show up at closings or notary appointments pretending to be you. Sometimes they recruit accomplices to pose as notaries or title agents, making the whole operation look legitimate.

These fraudsters do their homework. They target owners who live out of state, have substantial equity, or own properties in counties with lax verification.

Picture this: You're retired in Arizona but own a rental property in Oregon. A scammer uses your information to refinance that Oregon property, walks away with $200,000 in cash from a refinance, and vanishes. You're stuck with a mortgage you never authorized and had no idea existed until the lender starts foreclosure proceedings.

Wire Transfer Fraud in Real Estate Transactions

This one's exploding right now. It's also the scariest because victims do everything they think they're supposed to do—and still lose everything.

Criminals hack into email accounts belonging to real estate agents, title companies, or attorneys handling transactions. They lurk there for weeks, reading every message, learning how people communicate, finding out closing dates and dollar amounts.

Right before closing—usually 2-3 days out—the hacker sends what looks like a legitimate email with "updated" wire instructions. It comes from an email address that looks almost identical to the real one. Maybe they change one letter or use a similar domain name. The message matches the writing style of previous communications. It includes urgent language about last-minute banking changes.

The buyer, expecting final wire instructions, sends $175,000 to the account listed. Seems legit. Except it's not the title company's account—it's the criminal's.

By the time everyone arrives at closing and realizes the money never reached the escrow account, those funds have bounced through four different banks, gotten converted to cryptocurrency, or been wired overseas. Recovery? Nearly impossible. And here's the brutal part: since the buyer authorized the transfer, they often eat the loss.

Author: Daniel Crosswell;

Source: redmonpestmgt.com

Foreclosure Rescue and Loan Modification Scams

When you're drowning financially and facing foreclosure, you'll grab any lifeline. Scammers know this.

These operations contact homeowners through foreclosure notices (which are public record), promising to stop foreclosure or slash mortgage payments. They charge upfront fees—anywhere from $2,000 to $10,000—for "services" they never actually perform. Legitimate HUD-approved housing counselors provide the same help for free, but desperate homeowners don't always know that.

Here's a particularly cruel variation: The scammer convinces you to transfer your deed to them "temporarily" while they "negotiate with your bank." You stay in the house as a renter. They promise you'll get the deed back once everything's sorted out.

What really happens? They refinance your property, pocket the equity, stop making payments, and ghost you. You get evicted from a house you no longer legally own, yet you're still responsible for the original mortgage. It's devastating.

Some scams tell homeowners to stop communicating with their lender entirely and send all payments to the "rescue company" instead. While the homeowner thinks negotiations are happening, foreclosure proceeds on schedule and the scammer keeps every payment.

How Real Estate Fraud Schemes Actually Work

Let me walk you through exactly how these scams unfold. Understanding the mechanics helps you spot them.

Wire Fraud Interception Process:

Week 1-4 before closing: Hackers send phishing emails or plant malware that compromises accounts belonging to anyone involved in your transaction—agents, title companies, attorneys. They gain access and just watch. They're reading everything. Learning your communication style. Noting your closing date and down payment amount.

Days 3-5 before closing: You're expecting wire instructions any day now. That's when the fraudster strikes. An email arrives from what looks like your title company's address. But look closer—maybe it's "titlecompany1.com" instead of "titlecompany.com." Or "ti†lecompany.com" with a special character that looks like a regular letter.

The message says something like: "Our bank just notified us of a system upgrade. Please use these updated wire instructions for your closing on Friday." Everything else in the email matches previous communications perfectly.

You wire $180,000 to the listed account, checking it off your closing prep list.

Within hours: Your money hits the fraudulent account and immediately scatters. Portion A goes to Bank #2. Portion B converts to Bitcoin. Portion C wires to an overseas account. Each movement happens within minutes.

Closing day: You arrive ready to sign papers. The title company asks where the wire is. You say you sent it three days ago. They check their account—nothing. Panic sets in. You pull up the email. That's when everyone notices the slightly wrong email address.

By now? The money's gone. It moved through so many accounts and jurisdictions that recovery becomes a legal and logistical nightmare. Most victims never get their money back.

Home Title Theft Mechanics:

The setup: Criminals browse public property records looking for ideal targets. They want properties owned outright (no mortgage monitoring), elderly owners (less likely to check records frequently), or out-of-state landlords (not watching closely). They compile personal information from data breaches, social media profiles, and public databases.

Document preparation: Using your information, they create convincing fake IDs—driver's licenses, passports, utility bills. They forge a deed transferring your property to themselves or a shell LLC they control. They either bribe a notary, impersonate one, or create completely fake notary stamps and signatures.

Recording the theft: The fraudster walks into your county recorder's office—or files online where available—with the forged deed and proper filing fees (usually under $100). The clerk verifies the document contains required elements like legal descriptions and notarization but can't confirm the signature is actually yours. The deed gets recorded and becomes the official property record.

Cashing out: Now holding a recorded deed "proving" ownership, the criminal approaches lenders for a cash-out refinance or home equity loan. They show up at closing with fake ID, sign loan documents, and receive a check for $150,000, $250,000, or whatever equity you've built up over years of payments.

The disappearing act: They take the money and vanish. Stop making payments. The lender starts foreclosure proceedings.

Your discovery: Months later, you receive foreclosure notices for a loan you never took out. Or maybe you try to sell and discover there's already a lien. Or worst case—someone shows up claiming they bought your house from the "new owner" and you need to leave.

Proving you're the legitimate owner requires lawyers, court battles, and months or years of stress—even when you ultimately win.

Author: Daniel Crosswell;

Source: redmonpestmgt.com

Foreclosure Rescue Scam Operation:

Finding victims: Scammers monitor public foreclosure filings, then bombard homeowners with mailers, phone calls, and even door-knocking. The pitch always emphasizes urgency: "Act in the next 48 hours or lose your home forever!" or "Secret program banks don't advertise!"

The hook: They promise to stop foreclosure, reduce payments by 60%, or negotiate with your lender. They claim special connections or proprietary programs. The fee? Usually $3,000-$5,000 upfront, payable only by wire transfer, prepaid cards, or cryptocurrency—payment methods with zero consumer protection.

Going dark: After you pay, they either do absolutely nothing or file pointless paperwork that doesn't actually help. They stop returning calls. Meanwhile, your foreclosure proceeds on the original timeline.

The deed transfer variation: In more elaborate versions, they convince you to sign over your deed "for protection" or "to refinance in our name since your credit is bad." You sign documents you don't fully understand, believing they're authorization forms. They're actually deeds.

The scammer records the deed, refinances to pull out your equity, pockets the cash, and stops paying. You discover you're now a tenant in your former home with no legal ownership—yet still responsible for the original mortgage debt. It's catastrophic.

Warning Signs and Red Flags to Watch For

You can spot most scams if you know what to look for. Here's what should make your alarm bells ring.

Communication irregularities top the list. Last-minute wire instruction changes—especially by email only—scream fraud. Real title companies establish wire details early and almost never change them. If instructions suddenly change, that's your red flag. Also suspicious: wire requests to personal accounts instead of established escrow accounts, or instructions coming from free email services (Gmail, Yahoo, Hotmail) rather than company domains.

Documentation problems reveal fraud in progress. Watch for unsigned papers, missing notary stamps, or signatures that look different across various documents in the same packet. Legitimate transactions generate mountains of consistent, professionally formatted paperwork. Photocopied signatures, documents with mismatched fonts within the same set, or forms with blank spaces that should have information all warrant serious scrutiny.

Pressure tactics are scammer bread and butter. They create fake urgency to stop you from thinking clearly or seeking advice. Statements like "this special offer expires at midnight," "don't involve your real estate agent in this," or "the bank forecloses tomorrow unless you sign today" are massive red flags. Legitimate professionals happily give you time to review documents, consult attorneys, and make informed decisions.

Unusual transaction structures often indicate something's wrong. Being asked to wire money to individuals rather than title companies? Red flag. Sellers who refuse to meet in person or insist on bizarre closing locations? Red flag. Deals structured specifically to avoid standard title insurance? Huge red flag. Cash-back arrangements where the seller secretly returns money after closing? That's literally mortgage fraud, even if both parties agreed to it.

Author: Daniel Crosswell;

Source: redmonpestmgt.com

Identity verification issues emerge when people avoid video calls, provide identification documents with weird inconsistencies, or claim they can't possibly appear at closing without legitimate justification. Sure, remote closings happen now. But completely dodging face-to-face or video contact throughout a $400,000 transaction? That deserves skepticism.

How to Detect and Prevent Real Estate Fraud

Protection isn't passive—you need active defense throughout your transaction.

Verify all wire instructions independently using phone numbers you personally look up on official websites or business cards you received in person. Never use contact information from email signatures or messages (those could be compromised). Call the title company directly before wiring anything. Confirm account details verbally. Better yet, use callback procedures where you initiate contact rather than answering incoming calls (which can be spoofed).

Implement secure communication practices by avoiding sensitive financial information in regular emails. Many title companies now offer secure portals for sharing wire instructions and closing documents. Use them. Enable two-factor authentication on every email account. Create strong, unique passwords. Remain skeptical of any message requesting urgent financial action, even when it appears to come from people you know and trust.

Work exclusively with licensed, vetted professionals—real estate agents, attorneys, title companies with verifiable track records. Check license status through your state's regulatory boards. Read reviews from multiple independent sources. Verify physical office locations exist and visit them if possible. Criminals frequently impersonate legitimate companies, so confirm you're actually working with real representatives, not imposters using similar names or copycat websites.

Monitor your property title through services that alert you whenever any document gets recorded affecting your property. Several companies offer this for under $20 monthly. Some homeowner's insurance policies now include title monitoring. You can also manually check public records online in most counties—do it quarterly if you own property outright or live out of state from properties you own.

Obtain owner's title insurance, which protects against losses from title defects, including certain fraud scenarios. Important distinction: lender's title insurance (required by most mortgages) only protects the bank, not you. Owner's policies protect your equity. That said, understand the limitations—some fraud scenarios aren't covered, particularly if you somehow contributed to the fraud through negligence or if the fraud occurred after you purchased the policy in certain circumstances.

Conduct thorough due diligence on properties and every party involved. Buyers should get professional inspections, title searches, and verification of seller identity and ownership rights. Sellers should verify buyer financial qualifications and be cautious with all-cash offers featuring rushed timelines that skip standard contingencies (sometimes legitimate, sometimes red flags).

Document everything by keeping copies of all transaction-related communications, documents, receipts, and notes. Take photos of identification documents shown by anyone claiming to represent a company. Keep detailed notes of phone conversations including dates, times, participants, and what was discussed. This documentation becomes invaluable if fraud occurs and you need to prove your actions to law enforcement, insurance companies, or courts.

Author: Daniel Crosswell;

Source: redmonpestmgt.com

Legal Consequences and Financial Impact of Real Estate Fraud

The fallout from real estate fraud extends far beyond immediate money losses.

Criminal penalties for perpetrators are severe. Federal charges under wire fraud statutes carry up to 20 years in prison. Bank fraud? Another 30 years possible. Aggravated identity theft adds mandatory consecutive sentences—meaning they run after, not alongside, other sentences. The FBI and Department of Housing and Urban Development actively investigate property fraud, especially schemes touching federally insured mortgages or crossing state lines.

State prosecutors pile on charges including forgery, grand theft, recording false documents, and conspiracy. Many states have penalty enhancements when crimes target elderly victims or involve amounts over certain thresholds ($50,000, $100,000, etc.). Real estate professionals who participate in fraud lose their licenses, face professional sanctions from industry organizations, and get sued civilly on top of criminal prosecution.

Financial losses for victims cascade well beyond the initial theft. Consider homeowners who lose property to title fraud—they often spend $30,000-$75,000 in legal fees over 2-4 years trying to recover ownership. Even winning doesn't erase the time, stress, credit damage, and inability to sell or refinance during that period. Buyers who wire money to fraudsters lose down payments they spent years saving. For many, it permanently ends their homeownership dreams.

Mortgage fraud victims face immediate loan acceleration (the entire balance becomes due right now), followed by foreclosure. If the property sells for less than what's owed, they face deficiency judgments for the difference. Credit scores tank—we're talking drops of 150-250 points. That affects future housing options, job prospects (many employers check credit), insurance rates, and more. Some victims file bankruptcy, losing additional assets beyond the fraudulently obtained property.

Recovery options exist but rarely make victims whole. Title insurance might cover losses up to policy limits, though gaps and exclusions often apply. Some homeowner's policies include identity theft coverage that helps with legal fees. Crime victim compensation programs in certain states provide limited reimbursement for specific expenses like counseling or lost wages.

Civil lawsuits against perpetrators, negligent professionals, or companies with security failures sometimes recover damages. But here's the problem: fraudsters typically have zero assets to satisfy judgments. You win the lawsuit and get a piece of paper saying you're owed $200,000 from someone who's disappeared or already spent everything. Class action suits against title companies or lenders with inadequate security have achieved settlements in some cases, though individual recoveries after legal fees are often modest.

Banks occasionally reimburse wire fraud victims as goodwill gestures, particularly when their own security failures contributed. But they're not legally required to in most cases. The faster you report fraud, the better your chance of freezing funds before they scatter beyond recovery. Report within 24 hours and you might—might—recover something. Wait a week and forget it.

We're seeing increasingly sophisticated criminal networks exploit technology to target vulnerabilities in real estate transactions. Your best protection is verification at every step. Don't assume an email is legitimate just because it looks professional. One phone call—using a number you look up yourself, not one provided in any email—can be the difference between closing on your home and losing your entire down payment

— Jennifer Martinez

Frequently Asked Questions About Real Estate Fraud

Can someone steal my house title without me knowing?

Absolutely, and it happens more often than you'd think. Criminals obtain your personal details from public records or data breaches, create fake identification in your name, forge your signature on a deed, and record it with the county. You might not realize anything's wrong until foreclosure notices arrive for loans you never took out, or until you attempt to sell or refinance and discover unauthorized liens.

Properties owned free and clear (no mortgage), vacation homes, rental properties, and houses owned by elderly individuals face the highest risk. Why? Because nobody's actively monitoring them. A mortgage company watches properties with loans, but if you own outright, there's no lender checking the title regularly. Title monitoring services alert you to recorded documents within days. You can also manually check county records online every few months to catch unauthorized activity early.

How do I verify wire transfer instructions are legitimate?

Never—and I mean never—rely solely on emailed wire instructions. Call the title company using a phone number from their official website, your agent's business card you received weeks ago, or directory assistance. Don't use any phone number from the email containing instructions (it could be part of the scam).

Verbally confirm every detail: routing number, account number, recipient name. Some title companies establish a code word early in the transaction that you must exchange before wiring funds—use it. If your title company permits it, send a small test amount ($10-$50) first, confirm they received it, then transfer the remainder.

Treat any last-minute changes to previously provided instructions with extreme suspicion. Verify through multiple independent channels. Yes, it's inconvenient. It's also the difference between closing on your dream home and losing your life savings.

What should I do if I suspect real estate fraud?

Speed matters enormously here. If you suspect wire fraud before sending money, stop everything immediately. Contact your bank's fraud department and the title company directly using phone numbers you verify independently.

If you already sent funds, you have maybe 24 hours to request a recall before the money scatters beyond recovery. Contact your bank immediately—don't wait until morning, don't wait until Monday. Then report the incident to the FBI through IC3.gov (their Internet Crime Complaint Center) and your local police department.

For title fraud or deed fraud, contact an attorney who specializes in real estate fraud right away. Notify your title insurance company if you have owner's coverage. File a police report to create an official record. Report fraud involving licensed real estate professionals to your state's real estate commission—they have authority to investigate and sanction licensees.

Document everything: save emails, print documents, screenshot communications, write down timelines while details are fresh. This evidence becomes critical for law enforcement, insurance claims, and potential civil litigation.

Does title insurance protect against fraud?

It depends on the type of policy and the specific circumstances. Owner's title insurance (which you purchase at closing for a one-time fee) protects against losses from title defects including certain fraud scenarios. Lender's title insurance (which your mortgage company requires) only protects the lender, not you personally.

Standard owner's policies typically cover losses from forged documents in the chain of title that existed before you purchased the property. However, coverage may not extend to situations where you contributed to the fraud or failed to take reasonable precautions. Some policies specifically exclude losses from fraud by someone who gained access to the property with your knowledge or consent.

The devil lives in the policy details. Read the actual policy—not just the summary—and ask your title agent specific questions about fraud coverage. Enhanced coverage options sometimes exist for additional premium. Also understand that title insurance generally doesn't cover wire fraud (money sent to scammers during your transaction)—that's a different category of crime.

Are foreclosure rescue companies always scams?

No, but the industry attracts scammers like flies to garbage, so approach with extreme caution. Legitimate help exists through HUD-approved housing counseling agencies, which provide free or low-cost assistance with loan modifications, short sales, and foreclosure alternatives. They charge nothing upfront.

Red flags for scams include: upfront fees before any services are performed, guarantees to stop foreclosure (nobody can guarantee that), requests to sign over your deed for any reason, instructions to stop communicating with your lender, and pressure to act immediately without time to review documents or consult an attorney.

Legitimate housing counselors never charge large upfront fees, never ask you to transfer property title under any circumstances, and actively encourage you to communicate directly with your lender. Before paying anyone anything, verify the company through your state attorney general's office, the Better Business Bureau, and HUD's list of approved counseling agencies. Better yet, start with a HUD-approved agency and skip the commercial "rescue" companies entirely.

How common is real estate fraud in the United States?

It's skyrocketing. The FBI reports real estate fraud as one of the fastest-growing financial crimes, with wire fraud in property transactions affecting thousands of victims annually. Reported losses exceeded $450 million in 2025 for real estate and rental fraud combined—and that's just what got reported. Many victims never file reports because they're embarrassed, don't realize certain losses qualify, or simply don't know where to report.

The American Land Title Association estimates title fraud attempts occur in roughly 1 in 10,000 properties each year, though rates vary dramatically by region. Metropolitan areas with high property values—think Los Angeles, Miami, New York, San Francisco—experience significantly higher fraud rates than rural counties. Fast-moving markets where everyone's rushing also see more scams.

Remote transactions, digital communication, and increasingly sophisticated hacking techniques have made certain fraud types (especially wire fraud) more prevalent. Simultaneously, increased awareness and better security measures have reduced other types. Bottom line: it's common enough that you need to protect yourself, but rare enough that basic precautions significantly reduce your risk.

Your home represents the biggest investment most people ever make. Real estate fraud threatens not just money, but stability, security, and dreams of homeownership. The schemes keep evolving as criminals adapt to new security measures and exploit fresh vulnerabilities.

But here's what they all have in common: deception, manufactured urgency, and exploiting trust. Protection requires active vigilance at every stage—buying, selling, owning, refinancing. Verify identities. Confirm financial instructions through channels you establish independently. Work with licensed professionals whose credentials you personally verify. Maintain healthy skepticism toward anything that feels rushed, unusual, or too good to be true.

Is making extra verification calls inconvenient? Sure. Does it feel awkward to question professionals? Sometimes. But compare that mild discomfort to the devastation of losing your home or life savings to fraud. One 5-minute phone call to verify wire instructions can save you $200,000 and years of legal battles.

Real estate transactions are complex by nature, involving multiple professionals, extensive documentation, large money transfers, and tight timelines. That complexity creates opportunities for fraud. But it also provides multiple checkpoints where alert participants can detect and stop schemes before they succeed.

Education transforms potential victims into protected property owners who recognize warning signs and take action before criminals gain traction. You've now got the knowledge. Use it. Verify everything. Trust but confirm. And when something feels off, it probably is—stop and investigate rather than proceeding under pressure. Your home is worth protecting.

Zoning regulations determine what you can build and where across the United States. This guide explains zoning law basics, classification types, how to find zoning information, navigate variances and permits, and address alternative structures like shipping containers

The Uniform Partition of Heirs Property Act prevents forced sales of inherited family land at below-market prices through mandatory appraisals, buyout rights, and partition in kind preferences. Twenty-nine states have adopted this reform legislation as of 2026

Trespassing represents one of the most common property violations in the US. Learn the legal definitions, differences between criminal and civil trespass, penalties, proper signage requirements, and how property owners can legally protect their land from unauthorized entry

Co-owning property with family members, business partners, or former spouses can become complicated when disagreements arise about selling, managing, or dividing the asset. When negotiations fail and co-owners reach an impasse, a partition action provides a legal remedy to force the division or sale of jointly owned real estate

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to real estate law, property rights, leases, liens, zoning, landlord-tenant disputes, and litigation.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal outcomes may vary depending on jurisdiction, property type, and individual circumstances.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified attorneys or real estate professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.